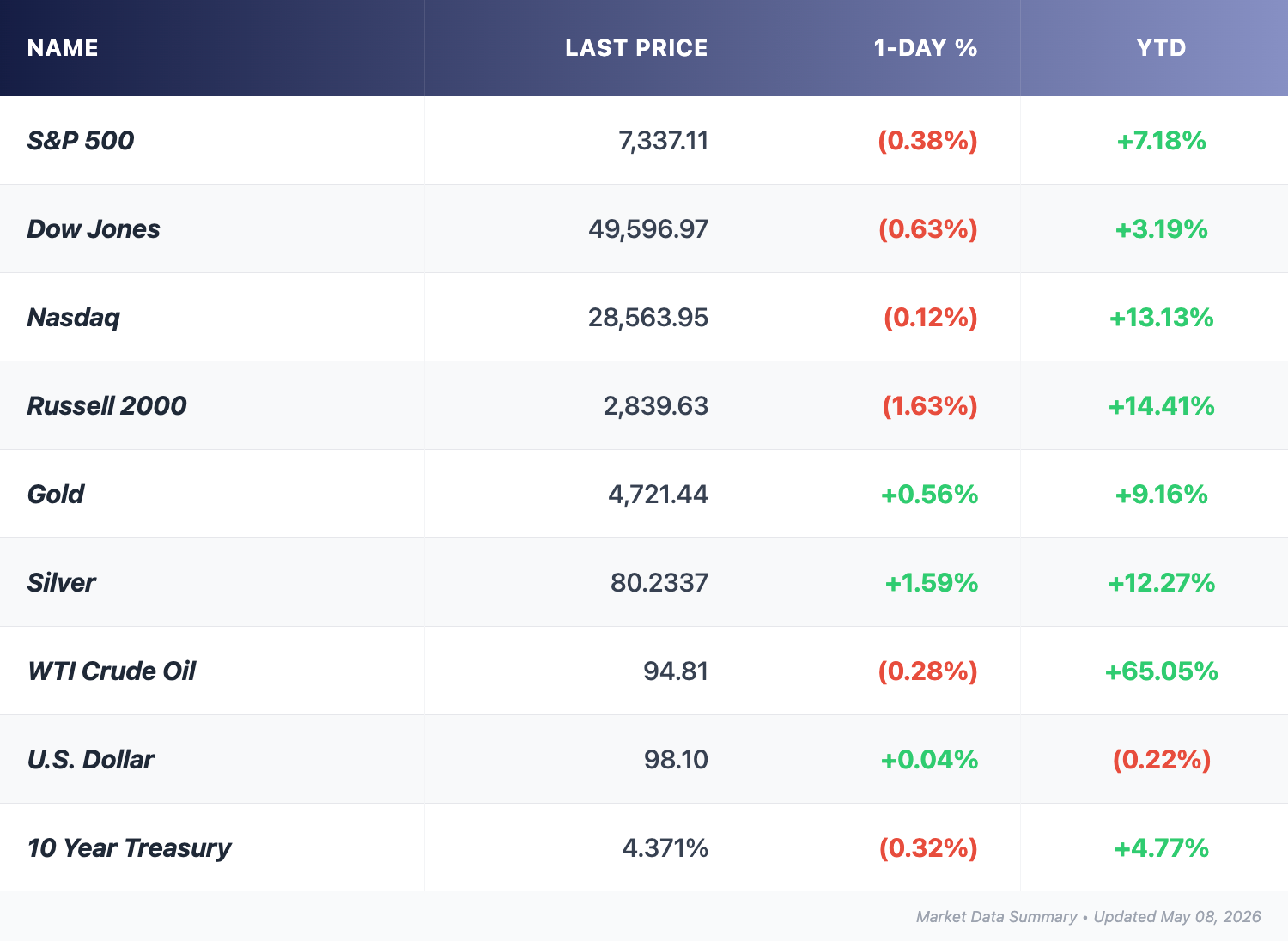

🔹 Stocks Pause, Gold And Silver Press On

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

Yesterday's records gave a little ground back today. A senior Iranian official pushed back on the US peace framework, oil whipsawed through the morning, and the major indexes stepped down from their highs. Beneath the surface, the picture is more layered. Earnings continue to land, gold and silver extended their rally, and a quiet handful of cyclical and tech leaders printed fresh all-time highs. For readers focused on retirement stability, the more useful read is not the day's drift, but how persistent the inflation conversation remains.

The Pulse

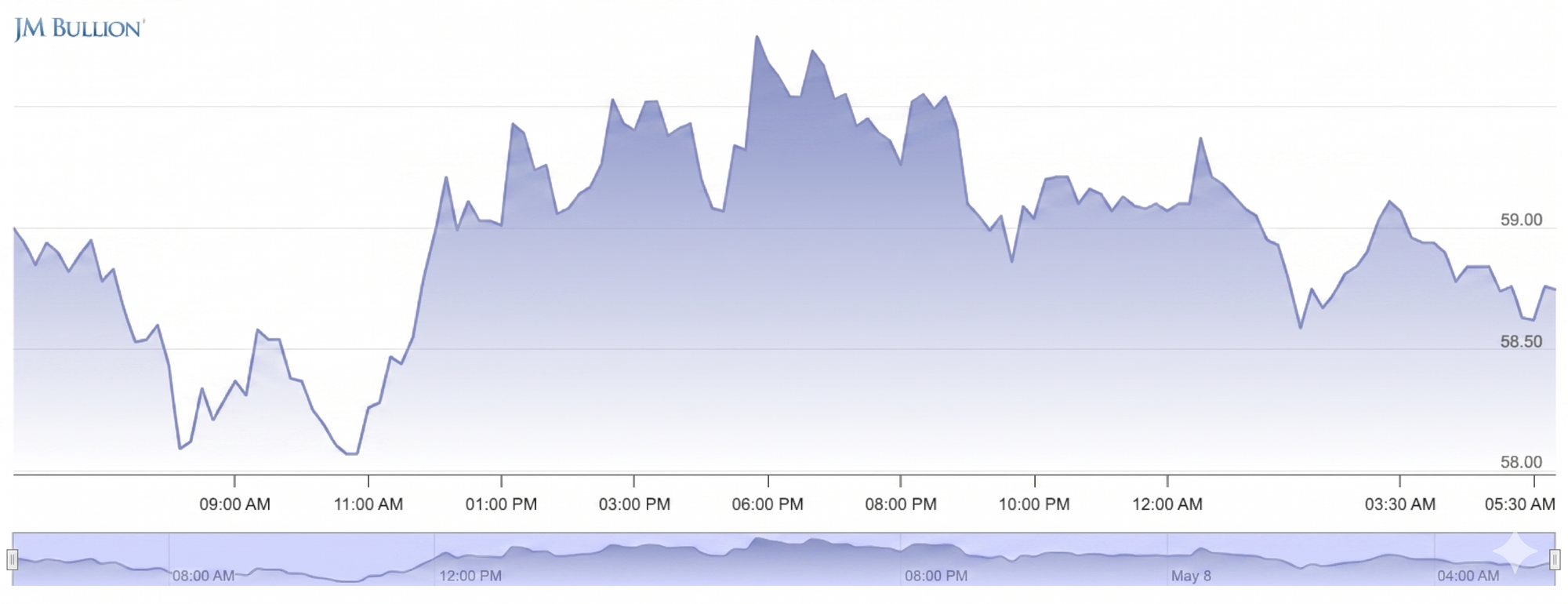

Gold rose for a third straight session, and silver gained more than five percent.

Markets

- The S&P 500 slipped after a fresh intraday high as semiconductor leaders took a breather, with Micron, AMD, and Lam Research each off about four percent.

- The Dow briefly crossed 50,000 for the first time since its February peak before pulling back into the close.

- WTI traded below $90 intraday before recovering to settle near $95 as Iranian official Mohsen Rezaei rejected the US peace framework as "unrealistic".

- Sixteen S&P 500 names traded at all-time highs intraday, including Alphabet, Apple, Caterpillar, and Intel.

The setup was the inverse of Wednesday's. Deal optimism stalled, semiconductors gave back some of their recent run, and energy held a firmer bid as the negotiation entered a harder phase. Breadth was uneven beneath the headline pullback. The strength in industrials and selected megacaps suggests the underlying tone is broader than the tape direction implied.

Earnings

- McDonald's set the morning tone. The chain posted its fourth straight quarter of US same-store sales growth, with revenue up around nine percent and adjusted earnings beating expectations. Even so, CEO Chris Kempczinski described "a challenging environment," and the stock fell to its lowest level in over a year.

- Shell topped profit estimates and raised its dividend by five percent, but trimmed its quarterly buyback to roughly $3 billion as it reallocates capital toward the balance sheet ahead of its ARC Resources close.

- Apollo Global crossed $1 trillion in assets under management for the first time, with record fee earnings, although a one-time tax charge produced a GAAP loss.

Gold & Silver Moves

Gold rose around one percent on Thursday to roughly $4,740 per ounce, its third consecutive higher session. The move tracked dollar softness and easing real yields, with investors growing more confident that diplomatic progress could cool oil-driven inflation pressures and reopen the Federal Reserve's rate-cut window. The structural bid remains intact. China's central bank logged its eighteenth consecutive month of gold reserve additions in April, reinforcing the official-sector demand floor.

TD Securities flagged a clear path above $5,200 once conflict-related inflation pressures fully fade. Whether gold gets there in a straight line is another question. The metal has been volatile in 2026, with sharp drawdowns interrupting its broader uptrend. What has not changed is the case for holding it.

Silver moved more decisively, rising more than five percent to roughly $81.55 per ounce, its highest close since mid-April. Industrial demand from solar and electronics, combined with the same monetary tailwinds lifting gold, gave silver its higher-beta role on the session. The relative performance is the point. Silver outpaced gold by nearly five to one today.

The Gold / Silver ratio compressed sharply to roughly 58.4, down from near 60 the prior session. That is well below the 80 to 90 range that has prevailed across most of the last decade, and meaningfully tighter than the readings that prevailed in the early phase of the conflict.

Sub-65 readings have historically coincided with environments where monetary demand for gold remains strong, but industrial and speculative demand for silver is even stronger. The current setup fits. Easing energy prices, when they hold, reduce headline inflation pressure and lift industrial activity expectations. Central bank gold accumulation provides a floor under the monetary leg.

For investors, the ratio offers two readings. First, silver looks relatively cheap to gold by long-term standards, though "cheap" is not the same as guaranteed to outperform. Second, a falling ratio typically signals improving risk sentiment alongside intact inflation hedging demand. Both readings are unusual in the same tape, and both fit today's price action.

For readers thinking about purchasing power across multi-year horizons, the precious metals complex is doing what it is supposed to do: holding value against currency softness while reflecting incoming changes in real activity.

The Deal Room

M&A / Investments

- Citigroup unveiled a multi-year $30 billion share buyback at its first investor day in four years, alongside higher long-term profitability targets.

- Secretary of State Marco Rubio approved $25.8 billion in air-defense interceptors and other weapons sales to Middle East partners.

- Sun Pharmaceutical is weighing financing options for its proposed $12 billion acquisition of NYSE-listed Organon.

IPO / Listings

- Defense intelligence satellite operator HawkEye 360 closed roughly 30% above its IPO offer in its NYSE debut.

Retirement Lens

Markets gave a little back today after a strong week. That happens. The discipline that builds retirement security rarely shows up in single sessions; it shows up in how a portfolio behaves across them. Investors who held through Wednesday's rally and Thursday's pause did not need to do anything different. The decision was already made.

The harder thread to ignore is the inflation story. Initial claims came in low. Productivity surprised to the downside. Unit labor costs accelerated. Consumer inflation expectations nudged up again in April. None of these prints is dramatic on its own, but the cumulative direction matters more than any single line. For readers in or near retirement, this is the environment to be honest about: a Federal Reserve with limited room, energy prices that can pop higher on any negotiation breakdown, and a labor market that is steady rather than soft. The portfolio considerations follow from there. Inflation-protected securities still earn their place. Money market funds continue to offer real yields that were unimaginable a few years ago. Intermediate-duration bonds reduce reinvestment risk without taking on the volatility of the long end.

The next phase of the Iran negotiation will tell us more than today's tape did. A confirmed agreement could ease energy prices and restore some flexibility to monetary policy. A breakdown would reintroduce the inflation question with new urgency. The practical posture is the same in both. Spread exposure across assets that behave differently when the headlines change. Hold enough cash and short-duration bonds to absorb a bad month without forcing decisions in equities. Keep a meaningful exposure to assets that hold value across cycles, including precious metals, where the recent move is doing exactly what those holdings are meant to do. Retirement portfolios are not built on bold calls. They are built on habits that survive both sets of headlines, the good and the bad. Today is one more data point in that longer story.

Headline Hunt

- Initial jobless claims came in at 200,000, with continuing claims at the lowest level in over two years.

- Q1 nonfarm productivity rose less than expected while unit labor costs accelerated.

- The NY Fed's April survey showed one-year inflation expectations rising to 3.6%.

- The US and Iran exchanged fire in the Strait of Hormuz late Thursday, with both sides accusing the other of striking first.

- IonQ rose about 9.5% after the quantum computing firm reported triple-digit annual revenue growth.

- Friday morning brings the April nonfarm payrolls report, with consensus pointing to a sharp slowdown in hiring.

- Brent crude held near $100 a barrel as Iran continued to assess the US peace framework.

- The labor share of nonfarm output fell to its lowest reading since the data series began in 1947.

- Treasury yields eased on the day as soft productivity and low jobless claims pushed back against any rate-hike concerns.