🔹 A hot jobs report reshapes the rate outlook while AI giants line up for Wall Street

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

Sometimes the market hands you a puzzle. A strong jobs report is good news, yet it nudged interest rate cuts further out of reach. Yields climbed, gold eased back, and stocks managed a quiet recovery after Friday's rough session. Meanwhile, the artificial intelligence story took a new turn, with two of its biggest names preparing to join the public markets. For anyone focused on retirement security, the theme today is patience: the economy is sturdy, but inflation is still doing the talking.

The Pulse

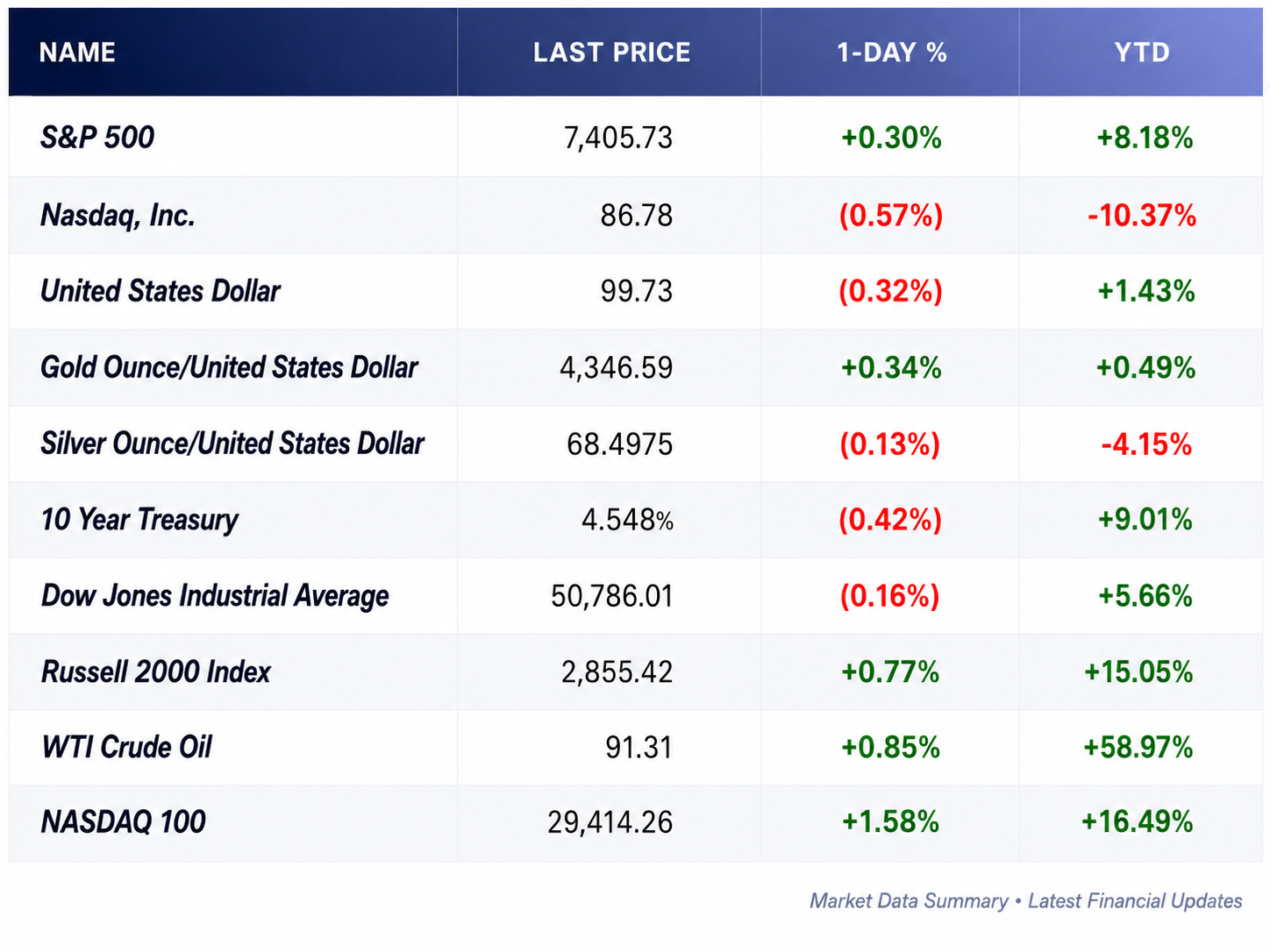

Two signals matter most today. First, Treasury yields. The 10-year sits near 4.55%, and the 30-year is back above 5%, a level that tends to ripple into mortgages, bonds, and savings. Second, energy. Oil stayed elevated, with U.S. crude near $91 a barrel after another Iran-Israel flare-up. Higher energy costs keep inflation warm, which keeps the Fed cautious.

Markets

- The S&P 500 rose 0.30% to 7,405.73, and the Nasdaq gained 0.86% to 25,929.66, as chip stocks rebounded.

- The Dow slipped 0.16%, closing at 50,786.01, the day's lone laggard.

- May payrolls jumped 172,000, well above the 80,000 forecast, pushing 30-year yields back over 5%.

- Oil settled higher, with Brent at $94.25 and WTI at $91.30, after intraday strikes threatened a fragile ceasefire.

Monday's rebound was real, but thin. Micron led the chip recovery, up close to 10% after Friday's drop. Still, the bigger story is the bond market. Strong jobs plus sticky inflation has quietly erased the case for rate cuts this year. Several major banks have dropped their cut forecasts entirely. For savers, higher yields are a mixed blessing: better returns on cash, but pressure on bond prices and borrowing costs.

Earnings

This is a quiet week between reporting seasons, so the calendar is light.

- Broadcom's recent quarter remains the reference point, with revenue of $22.19 billion, up 48%, and artificial intelligence chip sales up 143%.

- The lack of a raised outlook helped trigger last Friday's chip sell-off, a reminder that high expectations cut both ways.

Why it matters: when a leader posts strong numbers but cautious guidance, markets often punish the caution. That is the current mood in technology.

This week's lineup: Oracle reports June 10, with cloud growth the main focus and a fresh read on artificial intelligence spending.

Gold & Silver Moves

Gold traded near $4,332 an ounce, down about $76 from Friday. That is a modest pullback, and the year-over-year gain remains close to $951.

The interesting part is the why. You might expect gold to rise during a Middle East flare-up. Instead, it slipped. Two forces explain this. A firmer dollar and a sharp move higher in Treasury yields both make non-yielding gold less attractive in the short term. When real yields rise, gold often pauses.

But the longer story stays intact. Central banks bought an estimated 244 metric tons in the first quarter, above the five-year average. That steady official buying puts a floor under gold that short-term traders cannot easily remove. This is monetary demand, the kind tied to reserves and trust, not jewelry or factories.

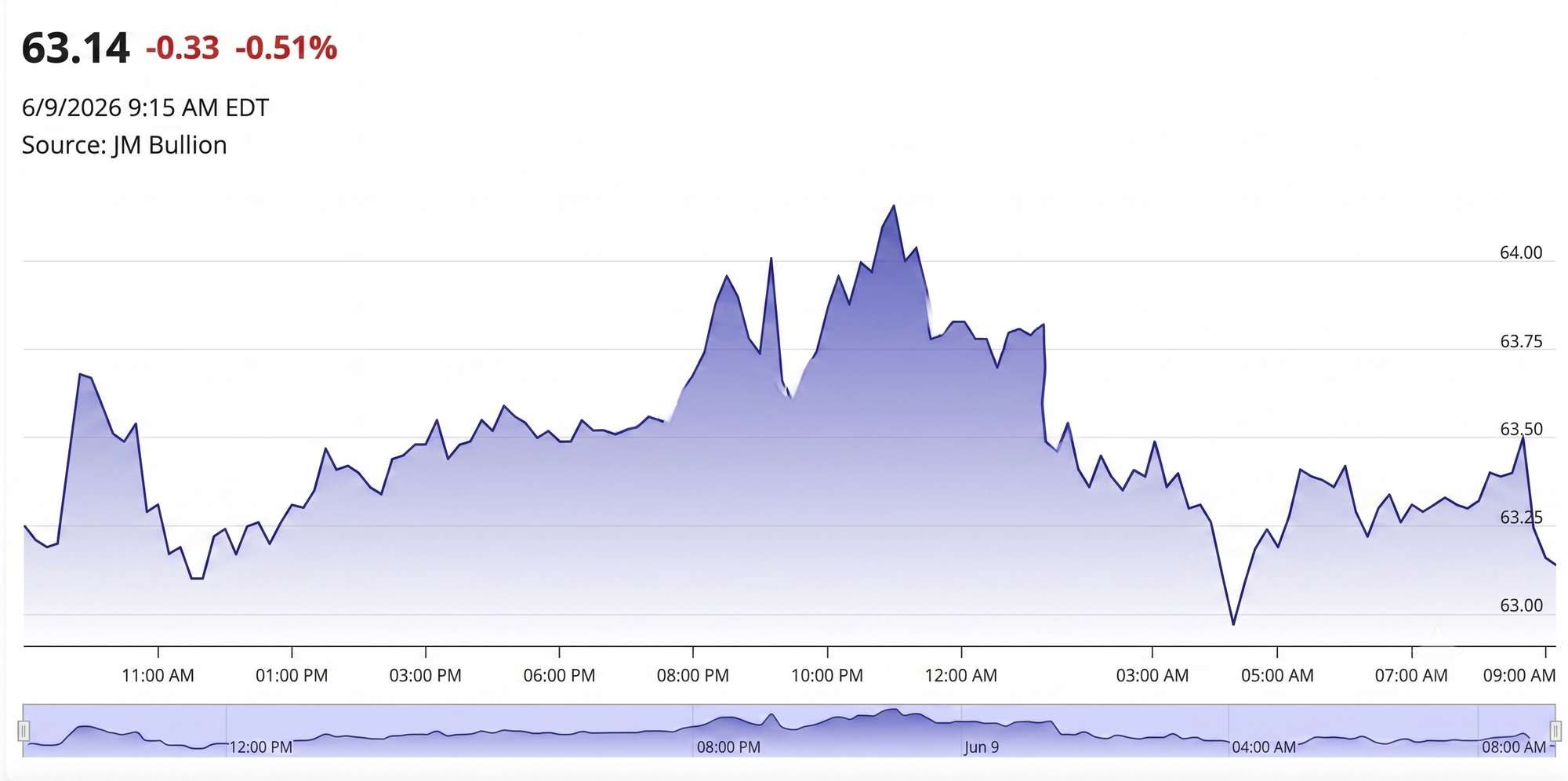

Silver opened around $74 an ounce, down roughly 1.8% to start the week. Silver tends to fall harder than gold on risk-off days, and it did again here.

Silver wears two hats. It is part safe haven, part industrial metal, used in electronics and solar panels. That second role makes it more sensitive to growth worries and more volatile than gold. After more than tripling over the past year, silver had room to cool.

Gold/Silver Ratio: Here is where the two metals tell a combined story. The ratio simply divides the gold price by the silver price. Today it sits near 58.5, or 4,332 divided by 74.

That is low by historical standards. The long-run average tends to fall between 60 and 70, and the ratio spiked above 100 during the panic of early 2020. A reading below 60 means silver is relatively expensive compared to gold.

What does a low ratio suggest? A few things. It points to silver's industrial premium being largely priced in, driven by clean energy demand, the artificial intelligence buildout, and tighter supply. It also reflects a market that has been leaning toward growth optimism rather than pure fear, since silver outperforms when investors feel confident. The recent move, with both metals easing but silver falling faster, has nudged the ratio slightly higher again. That hints at a small shift back toward caution, and toward gold as the cleaner monetary hedge.

The takeaway: for readers focused on preserving purchasing power into retirement, gold remains the steadier anchor, while silver offers more reward and more turbulence along the way.

The Deal Room

M&A / Investments

- Ingredion agreed to buy Britain's Tate & Lyle for $3.6 billion in cash, ending the firm's 87-year London listing.

- A consortium of Bouygues, Orange, and Iliad agreed to carve up France's SFR in a deal valued at $23.5 billion including debt.

- Amazon signed a multibillion-dollar agreement for Corning to supply optical fiber for its data centers, lifting Corning shares about 7%.

IPO / Listings

- OpenAI confidentially filed for an initial public offering after Monday's close, a week after rival Anthropic filed at a $965 billion valuation.

- Both companies could list as soon as the fourth quarter, setting up among the largest debuts on record.

Retirement Lens

Today rewards patience. Higher yields mean cash and newly issued bonds pay more, which helps income-focused savers. The flip side is that existing bond prices and rate-sensitive borrowing feel the squeeze.

Inflation is the thread running through everything, from oil to the Fed's caution. Gold's steady central-bank bid and its role as a monetary anchor remain worth understanding, even if the day-to-day moves look dull. Resilience, here, looks less like chasing the artificial intelligence rally and more like spreading risk, holding some ballast, and letting the strong economy do its slow work.

None of this is advice. It is context, so your own plan can stay grounded.

Headline Hunt

- The federal deficit widened by $294 billion in May, pushing the fiscal-year shortfall past $1.2 trillion.

- Markets have largely abandoned bets on a 2026 rate cut, with Citi a notable holdout expecting cuts from September.

- OPEC+ approved another July output increase of 188,000 barrels per day, despite Middle East supply risks.

- New Fed Chair Kevin Warsh faces a tricky path, with strong jobs and warm inflation pulling in opposite directions.

- Apple opened its developer conference with an artificial intelligence reboot of Siri, in Tim Cook's final event as chief executive.

- Bank of America strategists flagged the S&P 500 as expensive on 17 of 20 metrics, with tech dispersion the widest since 2000.

- The May unemployment rate held steady at 4.3%, signaling a labor market that has stopped weakening.

- Wage growth stayed contained, easing some fears that a rate hike is now certain.

- The Nasdaq's 4.18% drop last Friday was its worst session since the tariff turmoil of early 2025.