🔹 Bank Trading Beats, Chip Buyers Balk, Gold Firms

Strong bank revenue, expensive chip stocks, a firm bid in gold.

Good afternoon,

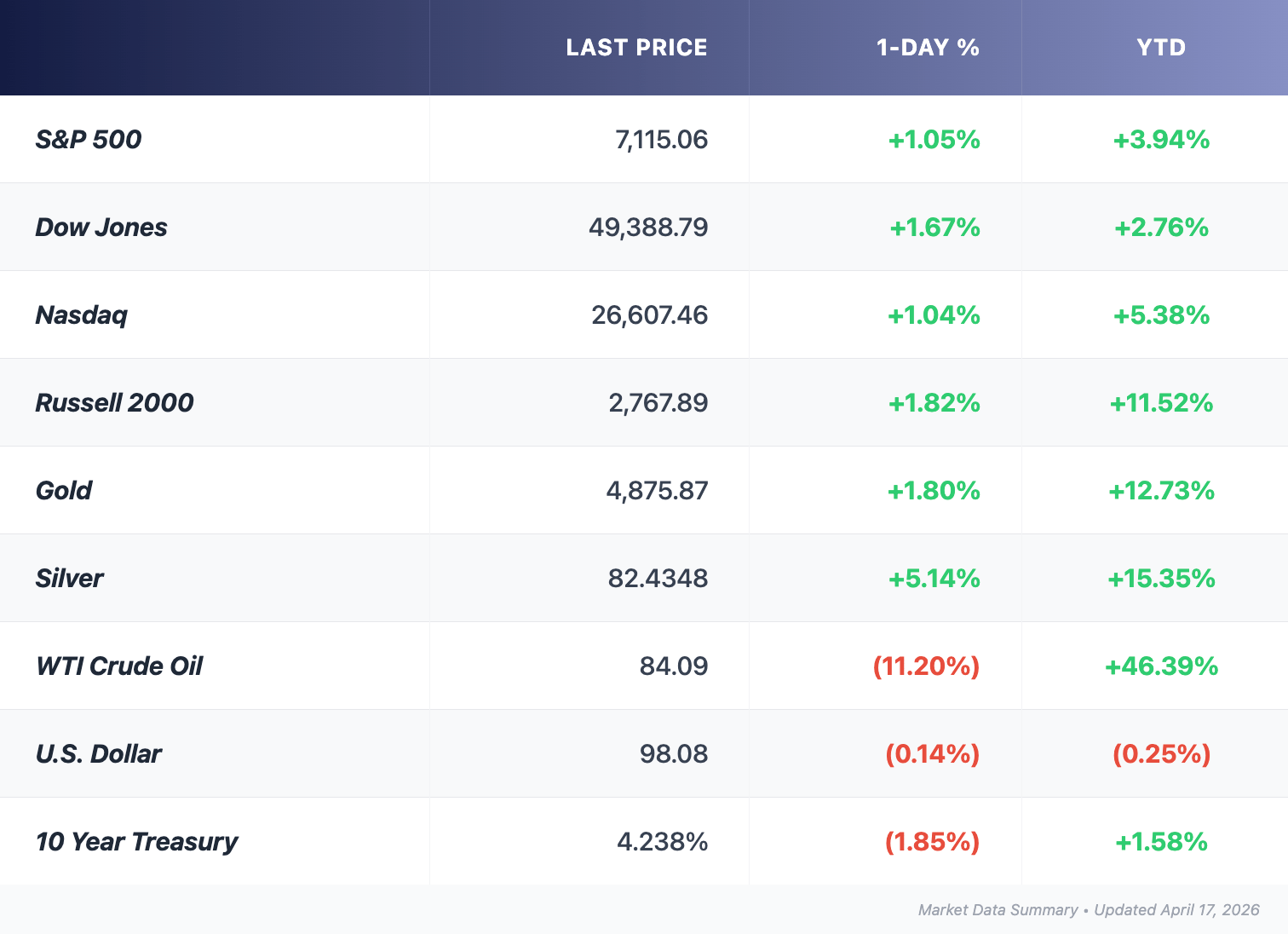

US equities closed Thursday at fresh records while oil stayed near $99 and gold pushed above $4,800. Bank earnings came in strong on trading revenue. Chip bellwethers beat estimates and still sold off. Today's issue works through what actually moved, what earnings signaled, and where the gold-to-silver ratio sits after silver's 30% rebound from the March low.

Getting started.

The Pulse

Markets

- Weekly jobless claims fell 11,000 to 207,000. The Philadelphia Fed manufacturing index jumped to 26.7, a 15-month high, but its prices-paid component surged to 59.3.

- Industrial production slipped 0.5% in March, missing consensus for a 0.1% gain.

- Fed funds futures now price the year-end rate in the 3.50% to 3.75% range, unchanged from December.

- Iran announced a coordinated transit route through the Strait of Hormuz during the Israel-Lebanon ceasefire, keeping flows restricted but not fully closed.

For income-oriented readers, the signal is in the spread. Short-dated Treasuries remain attractive at current levels. But the Philly Fed's prices-paid reading and oil above $90 mean real yields on longer maturities are narrower than headline rates suggest. That tension is worth watching.

Earnings

- Netflix led the afternoon. Q1 revenue of $12.25 billion beat consensus, adjusted EPS of $1.23 cleared the $0.76 estimate, helped by a $2.8 billion Warner Bros. Discovery breakup fee. Shares fell 9% after hours on weak Q2 guidance and the announced June departure of co-founder Reed Hastings from the board.

- TSMC Q1 profit rose 58% on AI chip demand. Revenue hit $35.9 billion. Shares still slipped roughly 3% as expectations sat higher than the print.

- Morgan Stanley reported record revenue of $20.58 billion and EPS of $3.43. Trading revenue beat by nearly $1 billion.

- ASML raised 2026 guidance to €36 to €40 billion. Shares fell 5% as China dropped to 19% of system sales from 36% in Q4.

- Charles Schwab reported adjusted EPS of $1.43 and client assets of $11.77 trillion.

Gold & Silver Moves

Gold:

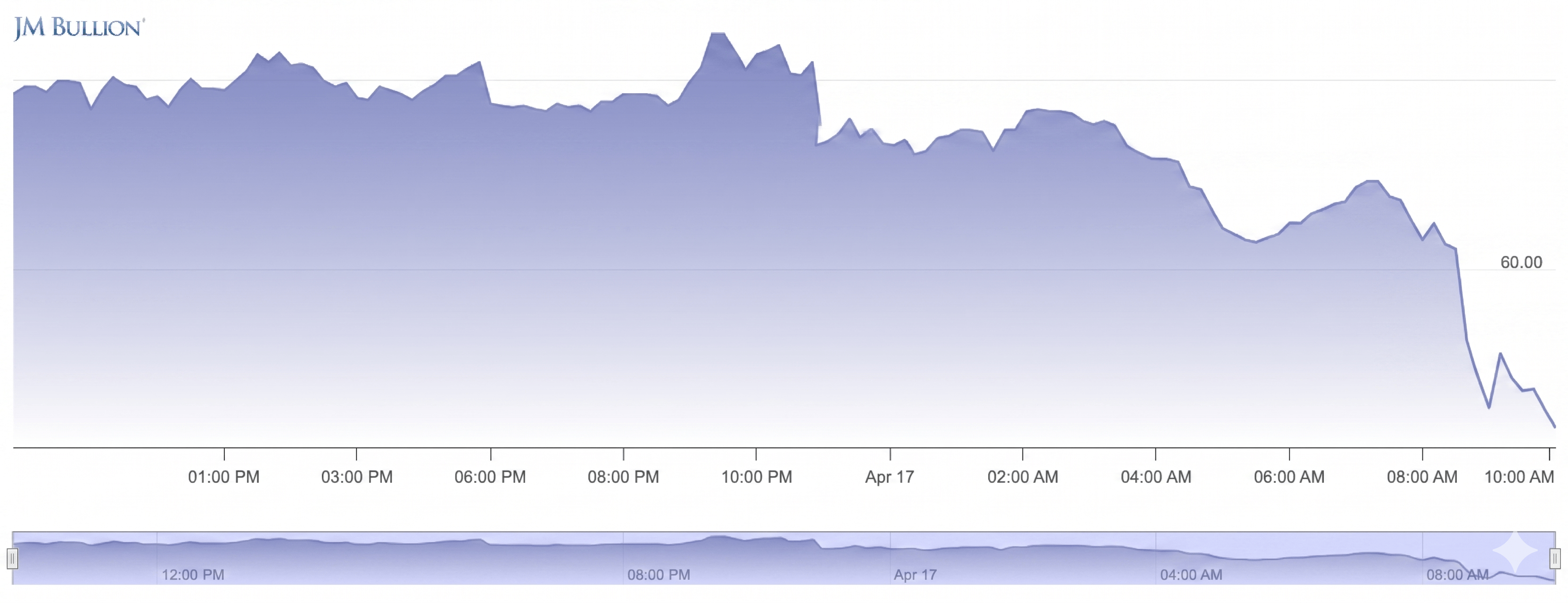

Gold closed Thursday at $4,818.89, up from $4,758.90 at the start of April and well off the March low near $4,382. Price is on track for a fourth consecutive weekly gain.

The recent move reflects two separate flows. Short-term, a weaker dollar (DXY near six-week lows earlier this week) and softer oil have supported the metal. Structural buying has not paused. JPMorgan models roughly 800 tonnes of central bank purchases in 2026. ETF holdings rose about 20 tonnes in April after the heaviest March outflows in five years.

Institutional year-end targets cluster between $5,400 (Goldman Sachs) and $6,300 (JPMorgan, Wells Fargo), with UBS at $5,600. These are not consensus forecasts but they indicate where large allocators are positioning.

Silver closed Thursday at $79.87, up about 4% for the week. It remains roughly 15% below where it traded when the Iran war began, and 35% below the January record high of $121.60. The Silver Institute and Metals Focus flagged a sixth consecutive year of structural deficit this week, projecting the 2026 gap at 46.3 million ounces.

The Gold / Silver ratio

That is below the long-term average of 70 to 75, and well below the 90-plus readings seen from 2022 through 2024.

A ratio near 60 historically means silver is trading expensive relative to gold. That can occur for two different reasons. The first is industrial: solar, electronics, and vehicle electrification pulling metal out of storage faster than mines can replace it. The second is monetary: investors using silver as higher-beta exposure to the same forces moving gold. Both are present in this cycle. Industrial fabrication is forecast to decline 3% in 2026, but supply is tightening faster, and coin and bar demand is forecast up 18% on a US retail recovery.

A ratio at 60 is not the extreme compression seen in January, when silver briefly spiked. It is also not the stretched reading from the 2022-2024 period when silver looked cheap against gold. The current level suggests the market is pricing silver as a working industrial metal with monetary properties attached, rather than a pure safe haven.

The takeaway

Gold and silver both ended the week higher while equities set records, an unusual combination that tends to appear when investors want growth exposure and purchasing-power hedges at the same time.

The Deal Room

M&A / Investments

- Amazon agreed to buy satellite operator Globalstar for $11.57 billion cash. Apple publicly endorsed the deal on April 16 (TechCrunch).

- American Industrial Partners will take Avanos Medical private for $1.27 billion at $25 per share.

IPO / Listings

- Madison Air Solutions priced the largest US industrial IPO since UPS in 1999, raising $2.23 billion at $27. Shares opened roughly 16% above the offer on Thursday.

Corporate / Distress

- Allbirds fell 36% Thursday after a 582% rally Wednesday on its "NewBird AI" pivot announcement.

Retirement Lens

A few observations worth noting, not acting on. Short-dated Treasuries continue to offer nominal yields above 4%, but Philly Fed prices-paid at 59.3 and Brent near $99 mean real yields are doing less work than the headline number implies. Inflation protection remains a live question rather than a settled one.

Bank earnings this week were boosted by trading revenue tied to Iran-war volatility. That revenue source is episodic, not structural. Dividend durability across the sector rests on net interest income, which moves with the yield curve.

The gold-to-silver ratio at 60 is neither extreme. Both metals have held their bid through an equity rally, which historically signals that buyers are hedging purchasing power rather than rotating between risk and safety.

Markets are sitting at records while an oil blockade, a coming ceasefire deadline, and an earnings bar that keeps rising are all unresolved. None of that is a forecast. It is the backdrop every reader will be reading the next batch of numbers against.

Headline Hunt

- The IEA estimates global oil supply fell 10.1 million barrels a day in March, the largest monthly disruption on record.

- BNP Paribas projects US GDP could grow more than 10% by 2034 on AI-driven productivity gains.

- Aluminum hit a four-year high in London on persistent Persian Gulf smelter supply concerns.

- Bank of America topped estimates Wednesday; CEO Moynihan described consumer banking as healthy.

- PepsiCo rose on stronger-than-expected revenue and earnings.

- Abbott Laboratories fell nearly 4% after guidance disappointed.

- Nvidia's new open-source quantum AI models lifted Asian software stocks, with several names hitting daily trading limits (BBG).

- Anthropic is reportedly fielding offers at an $800 billion valuation ahead of a potential October IPO (TradingKey).

Recommended Reading

- Why the stock market is hitting records despite Iran war (CNBC). Unpacks how the market is pricing a diplomatic resolution that has not yet happened, useful context for anyone weighing geopolitical risk in their holdings.

- TSMC and ASML post-earnings moves could signal what's to come. A practical look at why strong earnings are no longer enough when expectations run this high.