🔹 Cook Steps Aside. Warsh Steps Up.

Good afternoon,

A lot happened overnight, and most of it connects back to the same question: what does the price of energy do from here? The US-Iran ceasefire expires this week with no deal in sight, oil is back near $90, and the Fed's next chair faces senators today with inflation running at 3.3%.

Meanwhile, Apple announced its first CEO change in 15 years. Tim Cook, 65, is stepping aside after growing Apple's market cap from $350 billion to over $4 trillion. His successor, hardware engineering chief John Ternus, inherits a company facing an AI gap, tariff headwinds, and a foldable iPhone launch later this year. For anyone building around stability and income, weeks like this are less about reacting and more about watching where the pressure builds.

See also: How to Prosper in Trump’s New Economic Era partner

The Pulse

Futures are pointing slightly higher this morning, with S&P 500 and Nasdaq 100 futures up roughly 0.15% and 0.24%.

Markets

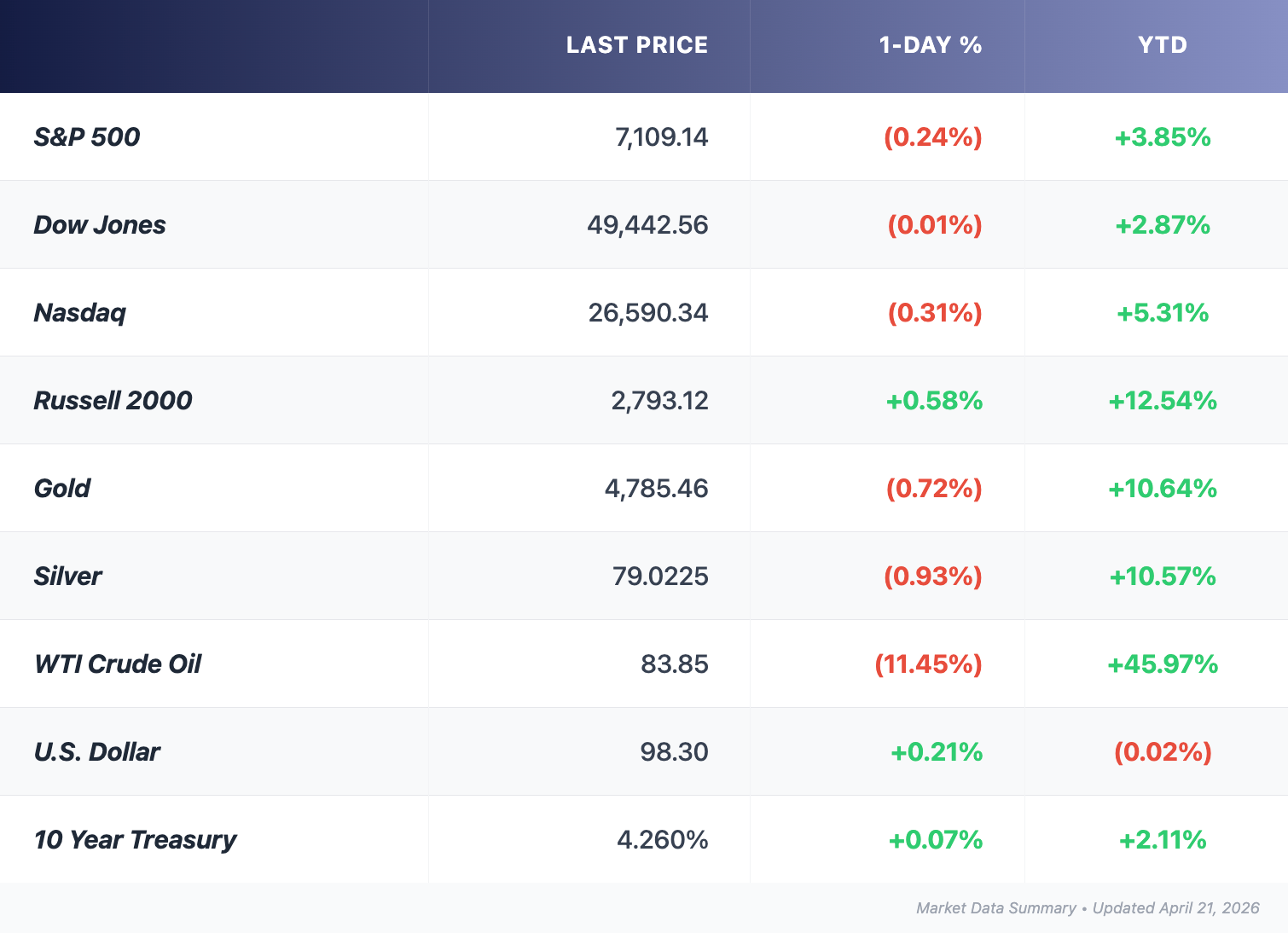

- Large caps pulled back on Monday. The S&P 500 fell 0.24% to 7,109.14, the Nasdaq dropped 0.26% to 24,404 (snapping its 13-day winning streak, the longest since 1992), and the Dow was essentially flat at 49,443, as weekend escalation between the US and Iran reversed Friday's relief rally.

- Small caps diverged. The Russell 2000 rose 0.58% to a new all-time closing record of 2,793, suggesting continued rotation into domestically focused names less exposed to global energy disruption.

- Apple named hardware chief John Ternus as CEO effective September 1. Tim Cook becomes executive chairman. Under Cook, Apple shares appreciated more than 1,700% and the company grew into a $4 trillion business. Ternus, 50, has spent nearly half his life at Apple and was instrumental in the development of the iPhone, AirPods, and iPad. His biggest challenge will be closing the gap in artificial intelligence, where Apple has lagged peers. Shares dipped less than 1% after hours.

The tension between geopolitical risk and earnings optimism remains the defining feature of this tape. Stocks have recovered from near-correction territory to all-time highs on the assumption that a deal gets done and the strait reopens. That assumption now faces a hard deadline.

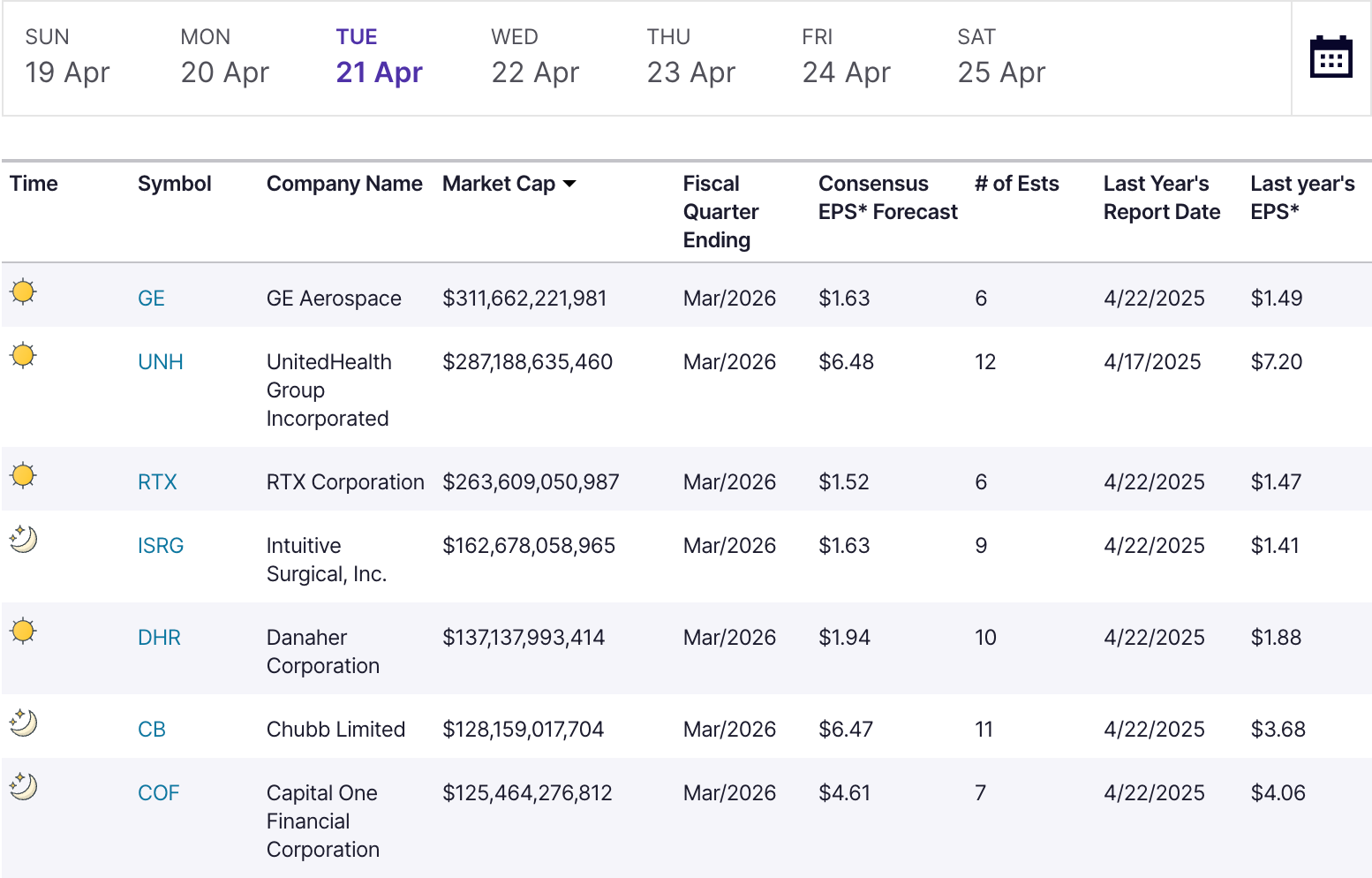

Earnings

- GE Aerospace also reports pre-market, with expectations of roughly 9% earnings growth and 18% revenue growth, supported by a $190 billion backlog. A strong read on aviation demand and aftermarket service revenue.

- Alaska Air withdrew its full-year profit forecast on Monday, citing elevated fuel costs from the Iran conflict, even as its Seattle-Tokyo route reached profitability within a year of launch.

- UnitedHealth Group reports Q1 results this morning. Analysts expect EPS of $6.60 on revenue of $109.7 billion. After a turbulent 2025 that included a medical care ratio increase of 340 basis points, investors will be watching closely for signs of margin recovery and Optum performance.

This one matters beyond Wall Street. UnitedHealth is the largest Medicare Advantage insurer in the country, covering millions of Americans over 65. Rising medical costs hit retirees directly, through higher premiums, reduced benefits, or both. How UnitedHealth manages its medical loss ratio is, in practical terms, a read on the affordability of healthcare in retirement.

This week's lineup:

- Today: UnitedHealth Group, RTX, Capital One, United Airlines

- Wednesday: Tesla, AT&T

- Thursday: Intel, Blackstone, American Airlines, American Express

- Friday: Procter & Gamble

Gold & Silver Moves

Gold traded at approximately $4,782 per ounce on Tuesday morning, down 0.8% from the prior session. The metal remains under pressure from a firmer dollar and rising Treasury yields, both driven by the Strait of Hormuz energy shock. Since the Iran war began on February 28, gold has dropped roughly 8 to 10 percent.

That decline might seem counterintuitive. Gold is supposed to thrive in geopolitical turmoil. But this conflict has created an unusual dynamic: an energy supply shock that raises inflation expectations, which in turn raises the likelihood of central bank rate hikes. Higher rates make non-yielding assets like gold less attractive. The war-trade has been a headwind, not a tailwind.

Still, physical demand remains firm. Central bank purchases have continued, and the metal sits well above $4,700 support. Historically, gold has tended to recover when rate-hike expectations ease, and a deal that lowers oil prices would shift that calculus quickly.

Gold's role in a retirement portfolio has never really been about short-term price swings. It's about what happens to purchasing power over decades. And with tax policy, inflation, and market structure all moving at once, how you hold physical gold inside a retirement account may matter just as much as whether you hold it at all.

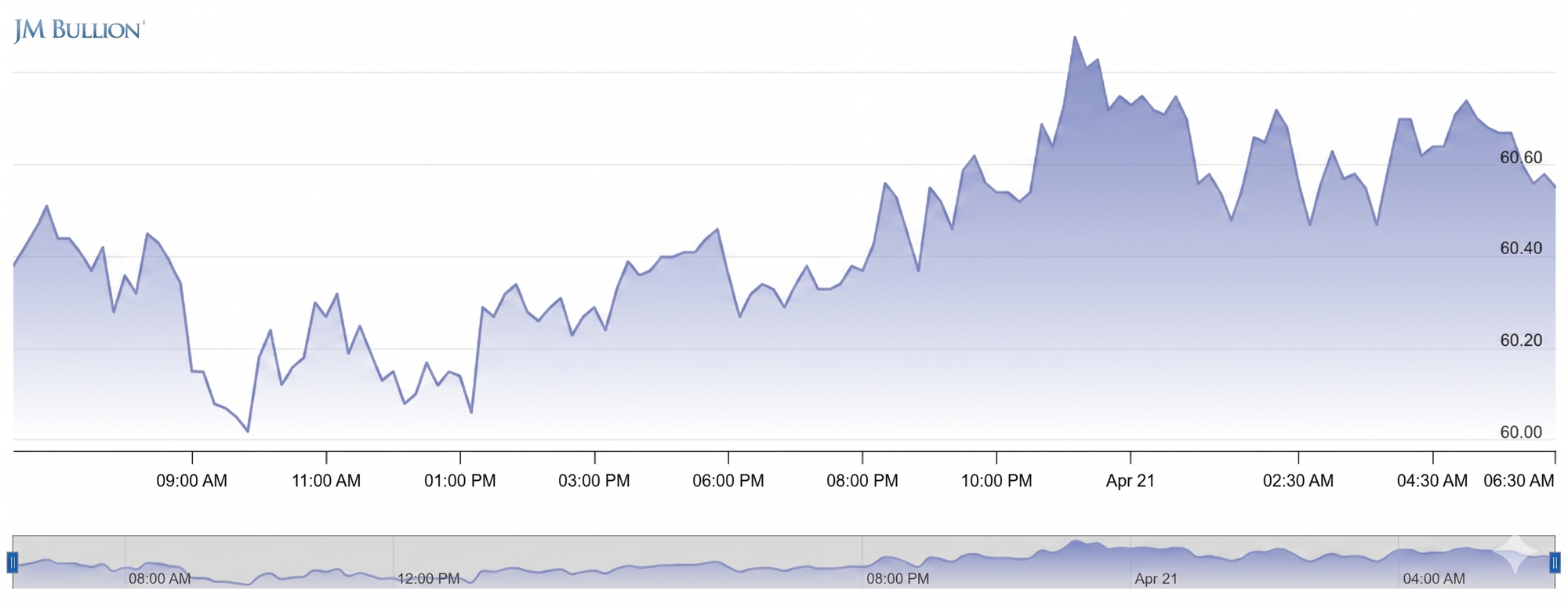

Silver eased to around $80 per ounce, pulling back slightly after a strong week. Silver is down roughly 15% from pre-war levels but sits nearly 30% above its March low. Its fourth consecutive weekly gain reflects a combination of monetary demand and robust industrial use in solar panels, electronics, and AI infrastructure.

What separates silver from gold right now is relative momentum. Over the past twelve months, silver has gained approximately 145%, more than triple gold's 43% return. That outperformance has compressed the gold/silver ratio to roughly 59.8.

The Gold / Silver ratio at ~60 is well below its historical average of 75 to 80, and far from the 90-plus levels seen in early 2025. A falling ratio generally means silver is gaining ground against gold, which tends to happen when industrial demand is strong and inflation expectations are rising but not yet choking off economic activity.

This ratio also reflects a shift in how investors view silver. It is no longer simply a monetary metal following gold's lead. Growing demand from the energy transition, particularly solar manufacturing, has tightened supply and created a structural bid. Six consecutive years of mining deficits have compounded the effect.

For context, the ratio briefly touched 60 during the 2011 silver spike and again in early 2021. Both were periods of strong commodity demand and reflationary expectations. The current reading sits in that same neighborhood, suggesting silver has narrowed its discount to gold, though it has not yet reached the extreme compression that historically preceded sharp reversals.

The takeaway: Both metals remain elevated by historical measures. In past environments with similar dynamics — high geopolitical risk, elevated energy prices, and compressed ratios — portfolios that included both metals tended to hold purchasing power more effectively than those relying on either alone.

The Deal Room

IPO / Listings

- Blackstone-backed Jersey Mike's filed confidentially for its IPO, with no pricing disclosed.

- Victory Giant Technology, an Nvidia PCB supplier, surged 60% in its Hong Kong debut after raising $2.6 billion, the city's largest IPO this year.

- Revolut CEO pushed the fintech's IPO timeline to at least 2028, saying public companies earn more institutional trust.

Retirement Lens

This is a week where long-term investors have historically benefited from discipline over action. Oil is volatile, the ceasefire deadline creates binary headline risk, and earnings season is just getting started. The UnitedHealth report this morning is worth watching closely, not for the stock price, but for what it reveals about healthcare cost trends that directly affect retirees.

The gold/silver ratio near 60 reflects an environment where both metals have played a role in preserving purchasing power. And the tariff refund process beginning this week is a reminder that policy risk can reverse as quickly as it arrives. Periods of uncertainty like this have historically rewarded patience and diversification.

Headline Hunt

- Kevin Warsh told senators the Fed "must stay in its lane" and pledged to fight inflation, with only one mention of employment in his prepared remarks for today's confirmation hearing.

- Trump said it is "highly unlikely" he would extend the Iran ceasefire if no deal is reached by this week's expiration, though the exact deadline has shifted between Tuesday and Wednesday in recent statements.

- Brent crude traded just below $95 per barrel, with WTI at roughly $88, as only a handful of ships crossed the Strait of Hormuz daily versus hundreds under normal conditions.

- Consumer prices rose 3.3% year-over-year in March, the highest since May 2024, driven largely by surging energy costs from the Iran conflict.

- Psychedelic drug stocks surged after Trump signed an executive order directing the FDA to accelerate reviews and allocating $50 million for research. Compass Pathways rose over 40%.

Share with Someone Who'd Value It

If you’ve found The Bull Investor useful, feel free to share it with someone in your circle—perhaps a colleague, a longtime friend, or a family member who takes an interest in their financial future.

We grow best through trusted recommendations, and your referral means a great deal.

Or copy and paste this link to others: thebullinvestor.beehiiv.com