🔹 Hot CPI Rewrites the Fed Playbook

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

April inflation came in hotter than expected, oil pushed past $100 again, and the bond market quietly began pricing in a Fed hike rather than a cut. Equities held up better than the headlines suggested, with the Dow even managing a green close. Beneath that, the calendar is full: Cerebras is days from a record-setting IPO, eBay slammed the door on GameStop, and Kevin Warsh moved one step closer to running the Fed. For readers focused on stability and income, the through-line is simple. The cushion for rate cuts has shrunk, and that matters for everything from bond ladders to gold allocations.

The Pulse

WTI crude jumped 4.2% to $102.18 a barrel as US-Iran talks stalled.

Markets

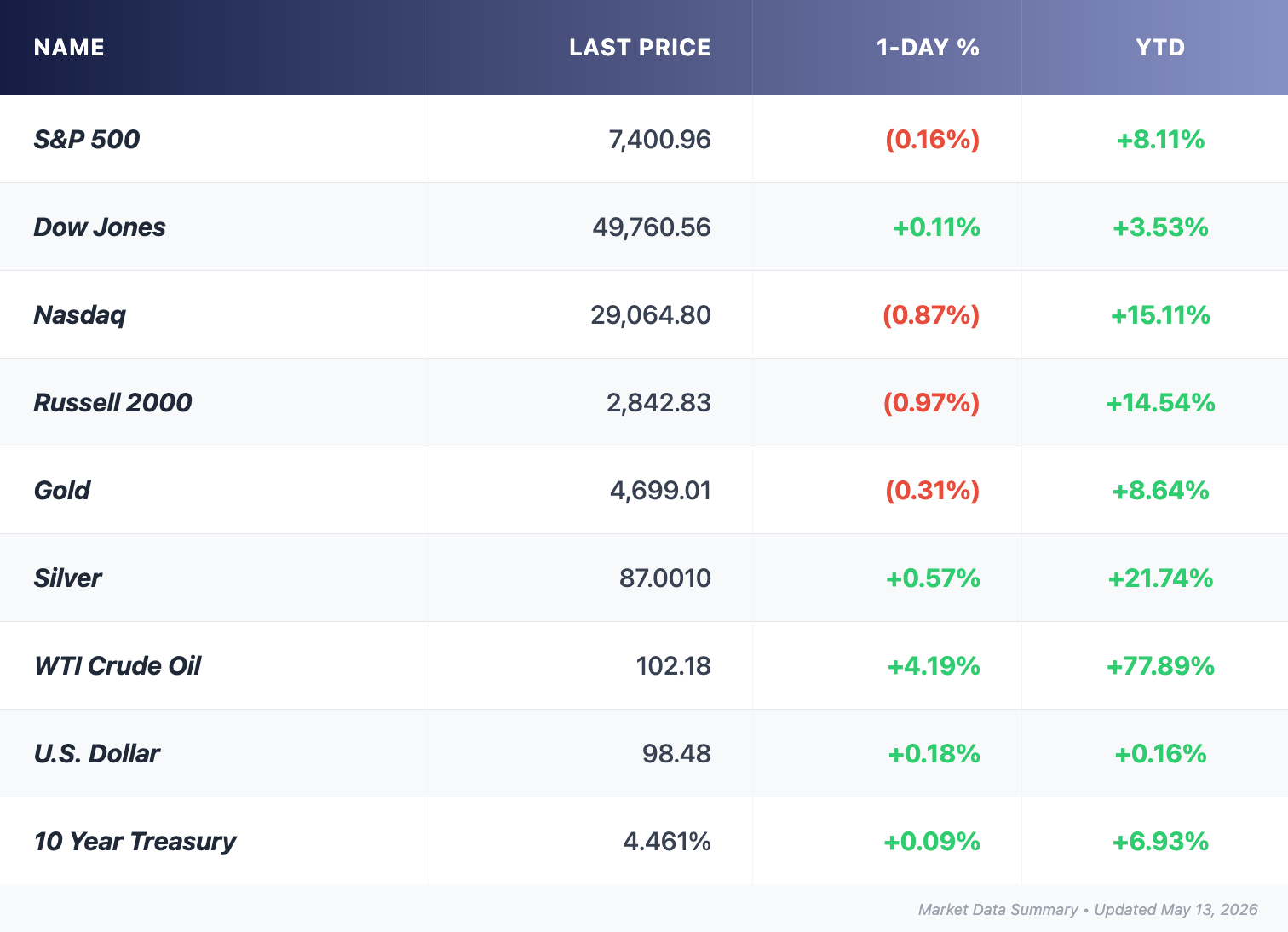

- S&P 500 slipped 0.16% to 7,400.96, weighed down by tech and discretionary names.

- Nasdaq fell 0.71% to 26,088.20, with chip leaders Micron, AMD and Qualcomm all declining after last week's rally.

- The Dow added 56 points to close at 49,760.56, supported by healthcare and staples.

- Rate expectations flipped: fed funds futures show better than a 1-in-3 chance of a hike by year-end, with cuts effectively priced out through 2027.

The session was a quiet repricing rather than a panic. Energy and defensives caught the bid, growth gave back some of its recent gains, and the bond market did the heavy lifting on the inflation message. For long-term portfolios, the takeaway is duration: longer Treasuries are no longer a one-way bet on falling rates.

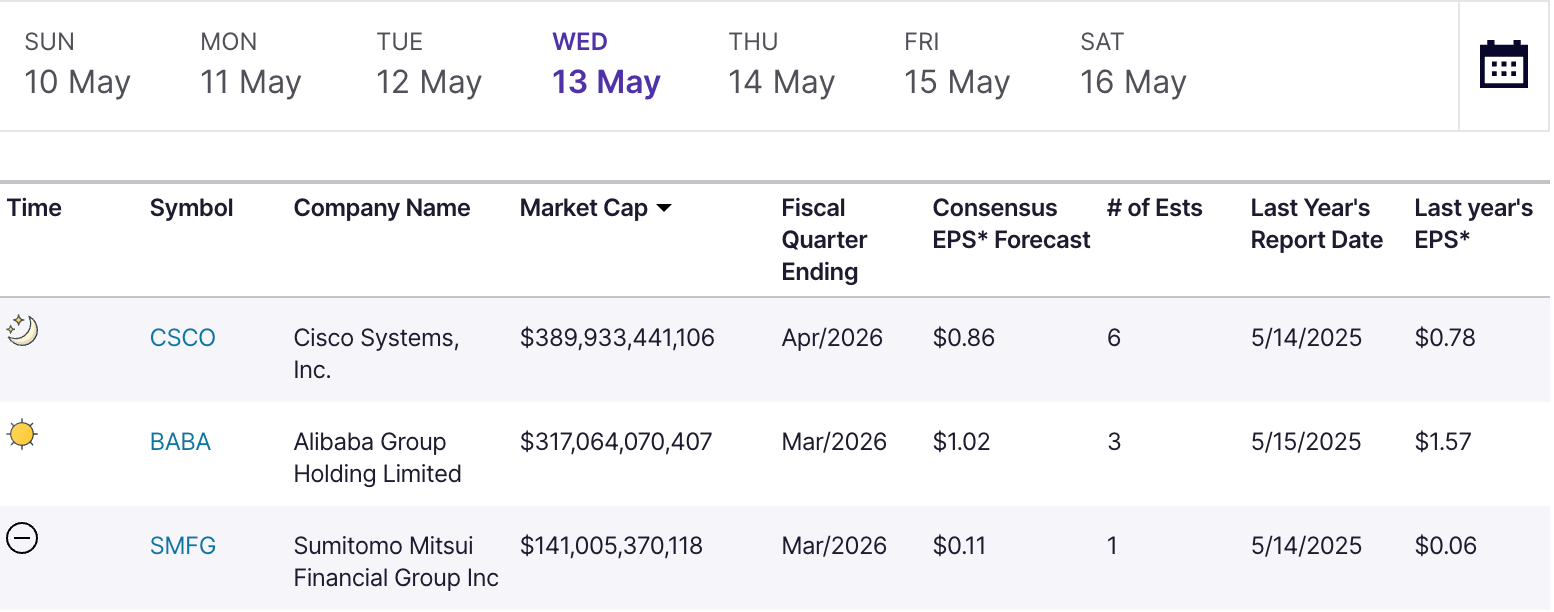

Earnings

- Saudi Aramco stole the headline. The world's largest oil producer posted adjusted Q1 net income of $33.6 billion, up 26% year-over-year, as its East-West Pipeline ran flat-out at 7 million barrels a day to bypass the closed Strait of Hormuz.

- On Holding beat on both lines, with Q1 sales of CHF 831.9 million (up 14.5%) and a raised full-year profit outlook.

- Hims & Hers dropped roughly 12% after the bell on weak Q2 EBITDA guidance of $35-55 million versus a $70 million consensus.

- GitLab fell 7% after announcing an agentic-AI restructuring that includes workforce cuts and a smaller geographic footprint.

The gap between energy producers and consumer discretionary is widening again. Sticky oil is a tax on households and a tailwind for upstream cash flows.

Gold & Silver Moves

Gold traded near $4,707 an ounce on Tuesday, down roughly $10 from Monday but still about $1,463 higher than a year ago. Prices remain well below the $5,589 all-time high set in late January.

The pullback is technical, not structural. A firmer dollar and the disappearance of near-term rate cuts have unwound some short-term positioning. Underneath, central bank buying has not slowed, and physical demand from Asia remains sturdy. The metal continues to do its job: it has tracked the inflation surprise and absorbed the geopolitical shock without surrendering its long-term trend.

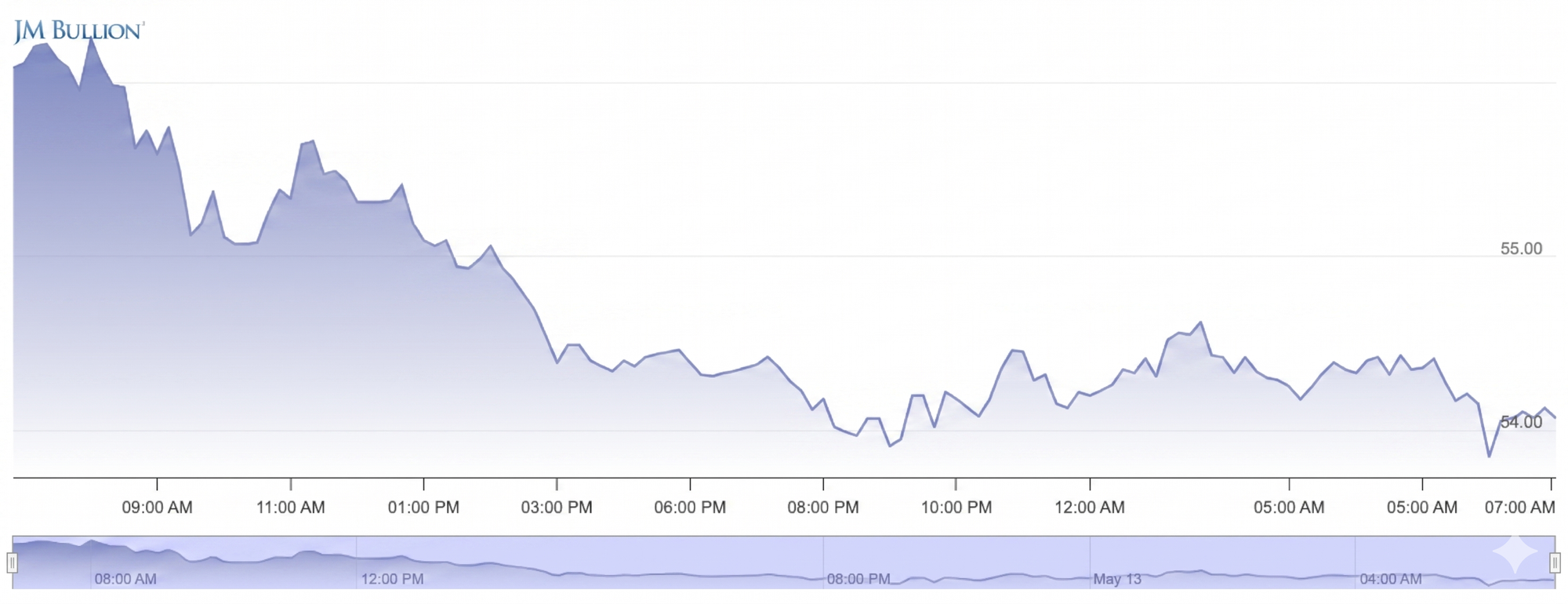

Silver closed near $84.53 an ounce after slipping more than 2% on the day, giving back part of Monday's 7% surge. Year over year, it has outperformed gold meaningfully, lifted by industrial demand from solar manufacturing and AI data-center buildouts, alongside a sixth consecutive year of supply deficit.

The Gold / Silver Ratio

At today's prices, the gold-to-silver ratio sits at roughly 55.7.

That is historically low. The long-run average is closer to 65-70, and the ratio spiked above 100 during the 2020 pandemic shock. A compression to the mid-50s tells us silver is expensive relative to gold, but the reason is informative rather than alarming.

When the ratio falls, it typically signals one of three regimes: risk appetite is rising, industrial demand is strong, or inflation expectations are being repriced higher. Right now, all three forces are in play. Industrial silver demand is at the wheel: solar panels, electrification, and data-center wiring are pulling physical metal off the market at a pace mine supply cannot match. Layered on top is the safe-haven bid from the Iran conflict and the dollar's recent firmness.

What does this mean for relative valuation? At 55, silver looks fully priced versus gold on long-cycle averages. Either gold catches up if the macro driver shifts back to monetary fear, or silver consolidates if industrial demand softens. The signal is balance, not extreme. For investors evaluating the metals as a pair, the ratio suggests adding gold on dips rather than chasing silver here.

The takeaway: in a year when cash interest rates have lost room to fall and inflation has reaccelerated, both metals continue to anchor purchasing power. The ratio's message is that the bid is broad-based, which is precisely what a retirement portfolio wants from a hedge.

The Deal Room

M&A / Investments

- eBay rejected GameStop's $56 billion bid, citing financing uncertainty and governance concerns; GameStop shares fell ~4%.

- Nelson Peltz's Trian is reportedly sounding out Middle East investors to fund a take-private bid for Wendy's, sending the stock up as much as 14%.

- Apollo Global is in talks to sell MidCap Financial Investment, a roughly $3 billion publicly listed BDC, where Q1 defaults rose to 5.3% from 3.9%.

IPO / Listings

- Cerebras Systems is guiding investors above its $150-$160 marketed range, on track to raise roughly $4.8 billion in the year's largest IPO; trading begins Thursday on Nasdaq.

Retirement Lens

The April inflation print is the kind of data that quietly resets long-term assumptions. With cuts off the table and a hike back on the radar, the case for short-duration bond income, dividend resilience, and a real-asset sleeve has firmed up. Gold is doing its job. Silver is doing more than its job. The ratio at 55 tells you both metals are working, just for different reasons.

For portfolios built around stability, the lesson of the day is patience. Sticky inflation is not a crisis. It is, however, a reminder that purchasing power needs a defender, and that hedge benefits should be earned through allocation, not timing.

Headline Hunt

- The Senate confirmed Kevin Warsh to the Fed board 51-45, with the chair vote expected Wednesday.

- Walmart is cutting or relocating about 1,000 corporate workers to consolidate AI and technology teams.

- US copper futures hit an all-time high above $6.40 a pound, up 40% year-over-year, on supply disruptions and AI data-center demand.

- WSJ reports SpaceX and Google are exploring a collaboration on orbital data centers.

- Aramco's CEO warned that the global oil market is losing roughly 100 million barrels of supply per week with Hormuz still impaired.

- Trump departs for Beijing this week, with Tim Cook, Elon Musk and Boeing's CEO joining the delegation.

- Two-year Treasury yields rose to 3.93% as the bond market braced for the inflation print.