🔹 Iran escalation, surging oil, and a hawkish Fed reshape the market landscape

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

Markets had been on a remarkable streak. Nine consecutive days of gains, fresh records across all three major indexes, and an AI trade that seemed unstoppable. Then the world reasserted itself. Iranian missiles hit Kuwait and Bahrain, oil surged toward $100, Treasury yields climbed, and the Fed's next move may now be a hike rather than a cut. Broadcom's earnings, while strong on paper, disappointed the crowd that wanted even more. For those of us building portfolios meant to last decades, days like yesterday are useful. They remind us what we're really exposed to.

The Pulse

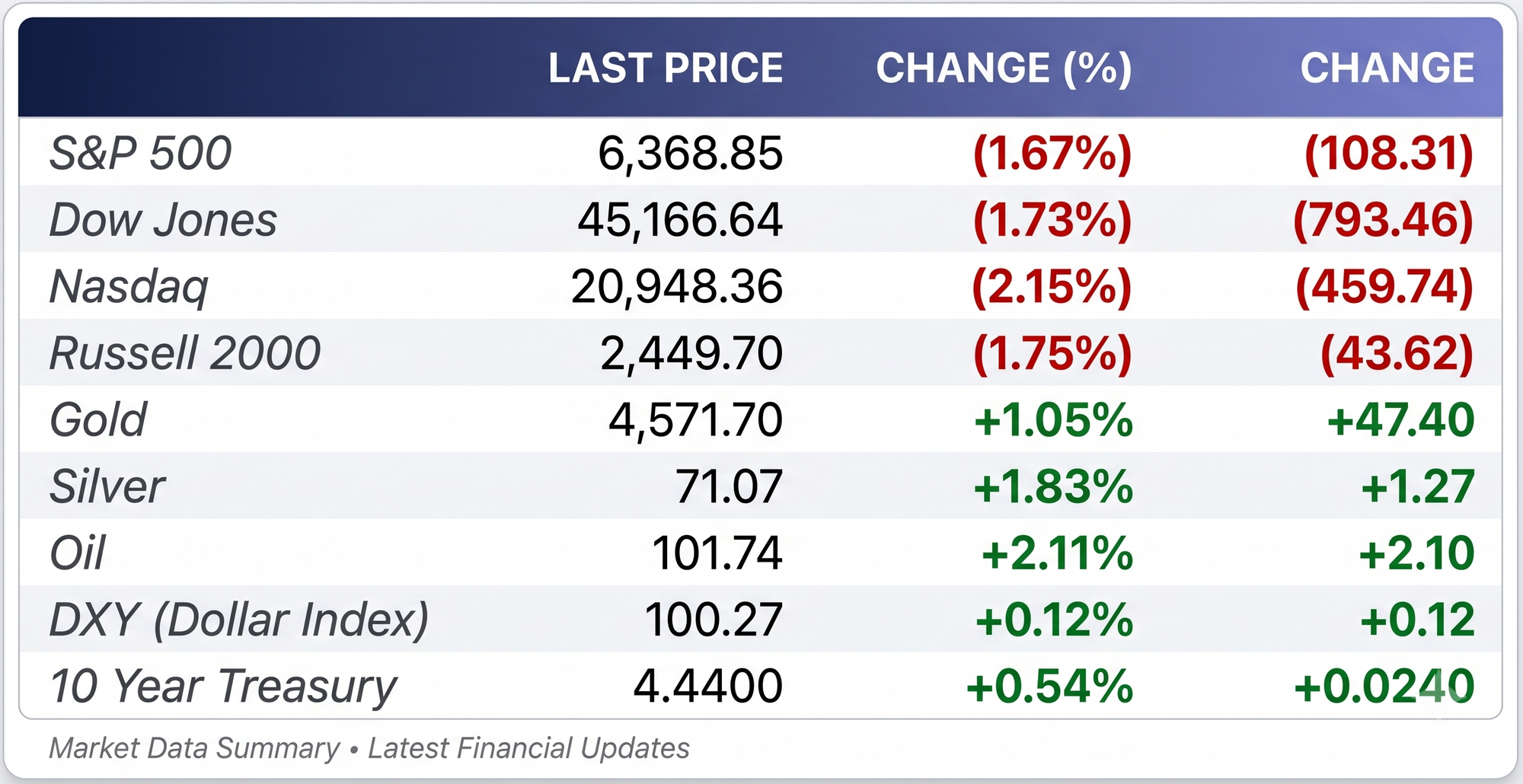

The 10-year Treasury yield rose to 4.48%. Brent crude closed near $98.80 a barrel. The S&P 500 snapped its nine-day winning streak, falling 0.74%. Futures this morning point to further weakness, with Nasdaq 100 contracts down 0.57% as Broadcom's after-hours slide ripples through Asia and into European trading.

Markets

- S&P 500 fell 0.74%, Dow dropped 621 points (−1.21%), and Nasdaq lost 0.89%, retreating from all-time highs as oil prices surged and Treasury yields jumped following Iranian missile strikes on U.S. bases in Kuwait and Bahrain.

- Brent crude rose 2.9% to $98.80/bbl and WTI gained 3.2% to $96.73, after the IEA warned global oil inventories could fall to critical levels ahead of peak summer demand.

- The ADP jobs report showed 122,000 private-sector jobs added in May, above the 117,000 consensus and the strongest reading since January 2025, reinforcing the view that the labor market is too resilient for rate cuts.

- The OECD's June Economic Outlook cut global growth to 2.8% for 2026 and warned of potential recession scenarios under a prolonged energy disruption, while revising G20 inflation upward by 1.2 percentage points to 4.0%.

The picture is getting more complicated. Strong jobs and stubborn inflation are pushing the Fed toward tightening, while geopolitical risk is pushing energy costs higher. For equity investors, the question is no longer just "how high can AI take us" but "what happens when oil and rates stop cooperating."

Earnings

Broadcom reported record Q2 revenue of $22.2 billion, up 48% year-over-year, with AI chip revenue surging 143% to $10.8 billion. EPS of $2.44 beat estimates. But shares fell roughly 14% after hours because CEO Hock Tan did not raise the full-year AI revenue target of $100 billion. The company also announced a 4-for-1 stock split.

- CrowdStrike posted Q1 revenue of $1.39 billion (+26% YoY), record net new ARR of $256 million, raised full-year guidance, and declared a 4-for-1 stock split. Shares still fell 10% after hours on soft Q2 revenue guidance.

- Hewlett Packard Enterprise surged 25% earlier this week after beating Q2 estimates and raising full-year guidance, marking its best single-day performance ever.

When a company beats estimates and still drops 14%, it tells you expectations had outrun reality. For long-term holders, the underlying numbers remain strong. But this is a market that punishes anything less than perfection in AI names.

This week's lineup: Costco, Veeva Systems, Ciena, and Medtronic still to report.

Gold & Silver Moves

Gold fell 0.8% on June 3 to $4,449/oz, weighed down by a stronger dollar, rising Treasury yields, and oil-driven inflation fears that pushed rate hike expectations higher.

That may sound counterintuitive. Gold is supposed to rise when the world gets more dangerous. But rising oil prices feed inflation expectations, which feed rate hike bets, which strengthen the dollar and lift yields. Gold pays no income. When yields climb, gold becomes more expensive to hold relative to Treasuries. That dynamic has dominated since late January, pulling gold from its peak above $5,000 down to the mid-$4,400s.

Central bank buying remains a structural support. Global central banks purchased 244 tonnes in Q1 2026 alone. But the near-term headwinds from monetary policy expectations are proving difficult to overcome.

Silver settled near $74.01/oz, also under pressure but holding up relatively well against gold. Silver carries an industrial demand component that gold lacks. Solar panels, medical devices, EVs, and data center infrastructure all consume silver physically. That dual role as both a monetary metal and an industrial input gives silver a different risk profile.

Gold/Silver Ratio currently sits near 60.1. This is calculated simply: divide the gold price by the silver price. At 60, the ratio has compressed meaningfully from prior years, when it traded above 80 during periods of extreme risk aversion. That compression reflects silver's extraordinary run in 2025, when it nearly tripled from $47 to above $116.

Historically, the ratio tends to rise when fear dominates, as investors flee to gold. It falls when growth and industrial demand favor silver. At 60, the ratio is neither stretched nor compressed. It sits near its long-term average, suggesting that the market currently views both metals as fairly valued relative to each other. For metals investors, a ratio persistently below 60 would signal silver gaining the upper hand, possibly driven by industrial consumption outpacing monetary demand for gold.

What the ratio tells us now is equilibrium. Neither panic nor euphoria. The market is pricing both inflation risk and real economic demand roughly in balance. If Middle East tensions resolve and industrial growth holds, silver may outperform. If the conflict deepens and rate hikes accelerate, gold could reassert its safe-haven premium.

The takeaway: Precious metals remain under pressure from the rate environment, but their role as a long-term hedge against purchasing power erosion hasn't changed. For retirement-focused portfolios, the current pullback from January highs may represent a more attractive entry point than the frenzy of early 2026.

The Deal Room

M&A / Investments

- Berkshire Hathaway agreed to acquire homebuilder Taylor Morrison for $6.8 billion in cash ($72.50/share, a 24% premium), Greg Abel's first major deal as CEO and a bet on long-term U.S. housing demand.

- People Inc. (formerly IAC) submitted a non-binding $48.30/share cash bid for MGM Resorts, valuing the casino operator at roughly $18 billion. MGM's board is reviewing.

- IFF agreed to sell its Food Ingredients business to CVC Capital Partners for $4.3 billion, retaining a 10% minority stake.

IPO / Listings

- SpaceX begins its investor roadshow today, targeting $75 billion at $135/share for the largest IPO in history. Nasdaq debut under ticker SPCX is expected June 12.

- Anthropic filed a confidential S-1 with the SEC on June 1, following a $65 billion Series H at a $965 billion valuation.

Retirement Lens

Days like yesterday recalibrate perspective. A nine-day rally feels comfortable. A 1.2% drop on oil and geopolitics feels alarming. Neither should drive decisions for portfolios built to last twenty or thirty years. What matters more is the structural picture: inflation is sticky, rates may go higher before they go lower, and the AI investment cycle is real but unevenly distributed. For retirement-focused investors, the priority remains diversification across asset classes, a steady allocation to inflation hedges including metals, and the patience not to chase a streak or flee from a pullback.

Headline Hunt

- ECB rate hike next week is now fully priced in after euro zone inflation accelerated in May.

- Bank of Japan faces 75% market-implied odds of a June rate increase.

- Alphabet upsized its equity raise to $84.75 billion from $80 billion after strong demand.

- Marvell Technology surged 25% after Nvidia's Jensen Huang said it could be the next trillion-dollar company.

- Constellation Energy priced an 11 million share secondary offering at $281/share.

- U.S. crude inventories dropped 6.8 million barrels, supporting oil prices ahead of summer demand season.

- Nvidia and Dell Technologies both fell more than 3% during Wednesday's session.

- Palo Alto Networks beat lowered Q3 estimates, rallying after an 80% run since late March.

- Alphabet fell nearly 4% on dilution concerns tied to the $84.75 billion equity raise.