🔹 POWELL HOLDS THE LINE. OIL DOESN'T.

Good afternoon,

The week opened with Fed Chair Powell doing something markets desperately needed: being boring. Speaking at Harvard on Monday, he made clear that the Fed intends to sit still and look through the oil shock rather than chase it with higher rates. That single message rippled across bonds, equities, and commodities. Meanwhile, the Wall Street Journal reported that President Trump has signaled a willingness to end the Iran campaign, even if the Strait of Hormuz stays closed. For investors focused on preserving purchasing power and building retirement income, the question this week is straightforward: does the end of shooting mean the end of inflation pressure? Probably not yet. But the direction of travel matters.

Getting started.

The Pulse

The 10-year Treasury yield fell 9 basis points to 4.3% on Monday after Powell's remarks, a meaningful move in bond markets. That eased some pressure on equities, but not enough. WTI crude settled at $102.88 per barrel, its highest close since July 2022. The tug-of-war between falling rate expectations and rising energy costs defined the session.

Markets

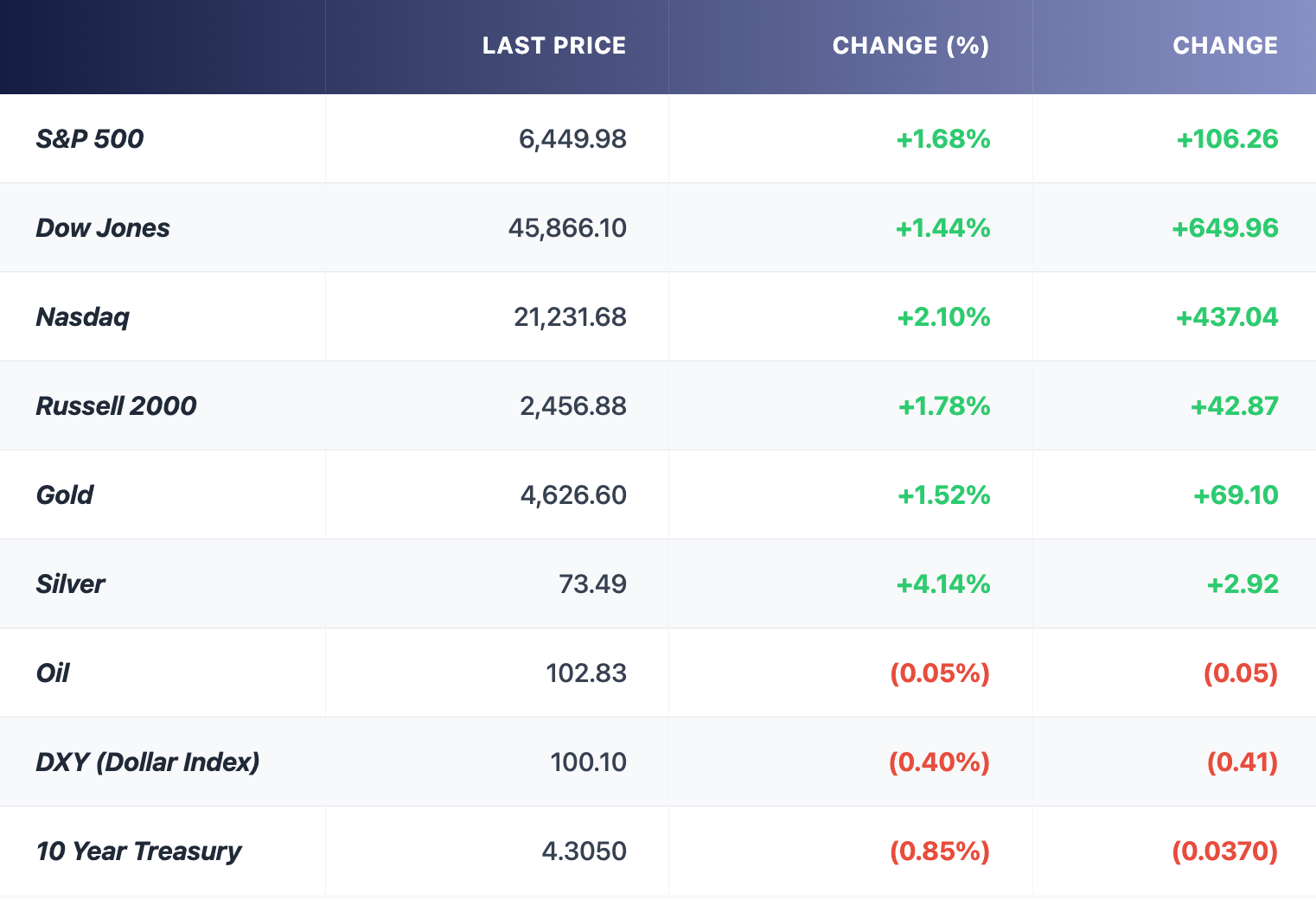

- The S&P 500 fell 0.39% to 6,343.72, now more than 9% below its closing high. The Nasdaq dropped 0.73%. The Dow squeaked out a gain of 49.50 points (+0.11%), propped up by financials and utilities.

- Treasury yields fell broadly after Powell said rate policy is "in a good place" and the Fed would look through the energy shock. The 2-year yield dropped over 8 basis points to 3.834%. Rate-hike odds for 2026 collapsed from over 50% to just 2.2%.

- Memory chip stocks extended their rout. Micron fell 9.88% on Monday, now down over 30% from its March 18 all-time high, as Google's TurboQuant compression algorithm raised questions about long-term memory demand. Sandisk and Western Digital dropped 7% and 8.6%, respectively.

- S&P 500 futures rose 0.8% Tuesday morning after the WSJ reported Trump told aides he would end the Iran war without forcing the Strait of Hormuz open, shifting the reopening burden to diplomacy and allies. Brent crude dipped below $107.

The market's central tension has not changed. Powell removed one fear, rate hikes, but the other, energy-driven inflation, remains very much alive. The S&P 500 sits just a few percentage points from correction territory. Less than 20% of its stocks trade above their 50-day moving averages. This is not a market that has found its footing. It is a market waiting for a reason to move, in either direction.

Earnings

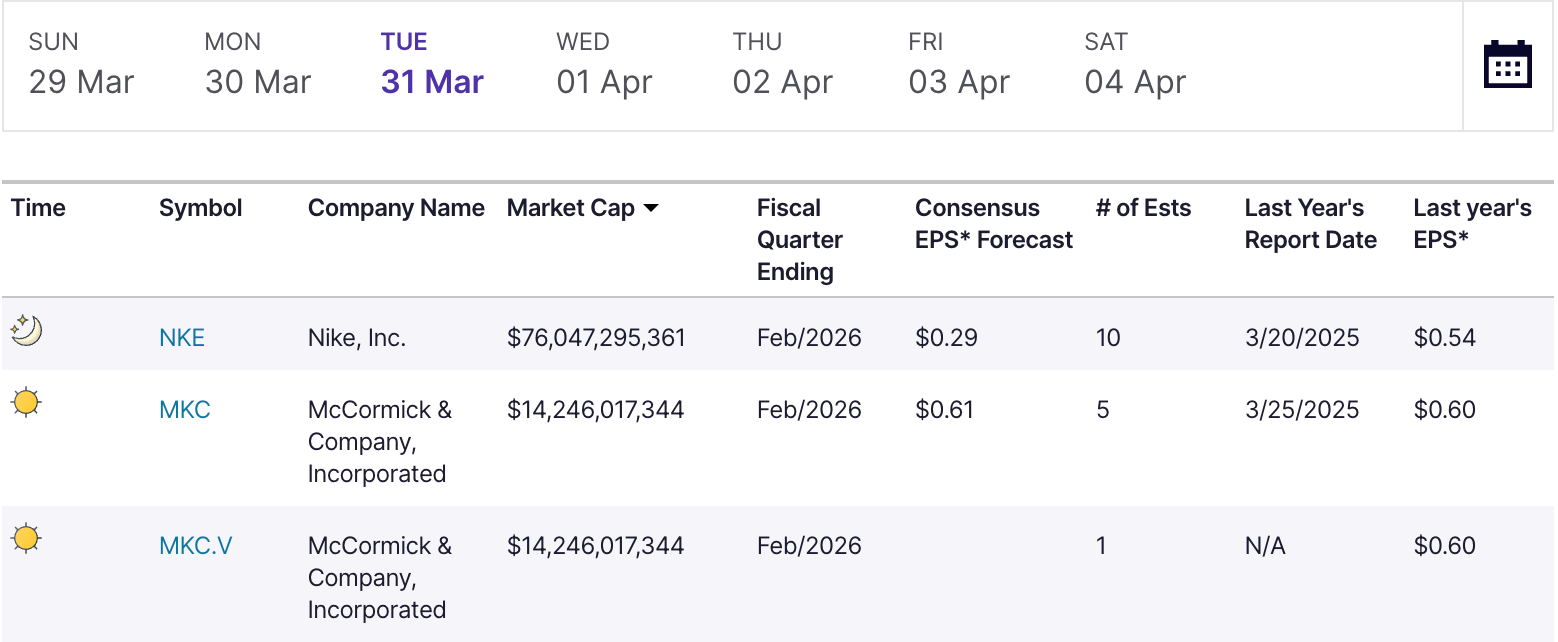

This is a relatively quiet earnings week, but today's headline report matters.

- Nike (NKE) reports Q3 FY2026 results after market close today. With consumer confidence falling and gas prices approaching $4/gallon, traders are watching closely for signs of weakening discretionary spending.

- McCormick (MKC) and Beyond Meat (BYND) also report this week, offering reads on staples pricing power and plant-based demand in a high-cost environment.

- Conagra Brands (CAG) reports Wednesday. Packaged food companies have been a useful barometer of consumer trade-down behavior.

Nike's guidance will set the tone. If the world's largest athletic brand flags a spending pullback, markets will listen. For retirement-focused portfolios, consumer staples companies on this week's calendar offer a quiet read on whether household budgets are starting to crack.

- This week's lineup:Today: Nike, McCormickWednesday: Conagra

Gold & Silver Moves

Gold:

Gold traded around $4,529 on Monday, with spot climbing approximately 1.5% to $4,579 in early Tuesday Asian trading. COMEX April futures rose to approximately $4,611. The metal is attempting a recovery after one of its most punishing months in memory. Gold is on track for its worst monthly decline since October 2008, yet it remains up roughly 5% for 2026.

The volatility is important to understand. Gold hit an all-time high near $5,595 at the end of January. By mid-March, it had fallen more than 20% from that peak, entering a technical bear market. The selloff was not driven by fading demand from central banks, the structural buyers that underpinned 2025's 66% rally. Instead, it was driven by momentum investors, hedge funds, and retail traders exiting crowded positions as rising Treasury yields and a strong dollar made non-yielding gold less attractive. SP Angel analyst Arthur Parish described it as "tourists" leaving the space, while the structural bid from sovereign buyers remains intact.

Powell's Monday remarks helped gold on the margin. By removing rate-hike expectations, he lowered the opportunity cost of holding gold. But the metal still faces crosscurrents: elevated Treasury yields (the 10-year remains at 4.35%, far above its pre-war level of 3.97%) and a dollar that, while easing, is still firm.

Silver:

Silver showed more life on Monday, trading around $71.19 in the morning before rising to approximately $73.20 in Asian trade on Tuesday, a move of roughly 3.7%. Silver has been more volatile than gold throughout this cycle. It surged 135% in 2025, suffered a historic 31% single-day crash in January when Trump nominated Kevin Warsh for Fed Chair, and has whipsawed since.

Silver's dual nature explains the divergence. It serves as both a monetary metal and an industrial input (electronics, solar panels, medical devices). When recession fears rise alongside inflation, silver gets hit from both sides: monetary demand weakens as yields rise, and industrial demand weakens on growth concerns. Its recovery on Tuesday suggests some easing of those pressures, but the path remains choppy.

The Gold / Silver ratio currently sits near 64, meaning it takes about 64 ounces of silver to buy one ounce of gold. This is well below the modern historical average of approximately 80, and it has compressed from higher levels as silver rebounded more aggressively this week.

What does a ratio in the low-to-mid 60s tell us? First, silver remains relatively expensive compared to gold by long-term standards. During periods of financial stress, the ratio typically expands, sometimes above 100, as investors flee to gold and away from silver's industrial exposure. The fact that the ratio remains compressed suggests markets have not fully priced in a deep recession, even with stocks in near-correction territory and oil above $100.

Second, the ratio reflects the unusual character of this moment: silver's industrial demand from AI, solar energy, and electronics has created a structural floor that did not exist in previous cycles. That floor limits how far the ratio can stretch, even when monetary conditions favor gold.

For metals investors, the current ratio suggests that silver is pricing in a more optimistic industrial outlook than equities are. That divergence is worth watching. If the economy weakens materially, silver could underperform gold, pushing the ratio higher. If the Iran situation resolves and growth stabilizes, silver could outperform further.

However, there is an asymmetry to watch. If ceasefire signals emerge and rate-hike fears ease, silver's industrial demand base could give it an edge over gold, potentially compressing the ratio back toward 55–60. Conversely, if the conflict deepens and recession fears take hold, gold's safe-haven premium could reassert itself, pushing the ratio toward 75 or higher.

The takeaway

Gold and silver are both recovering from a brutal month. For investors thinking about long-term purchasing power, the metals continue to serve their core role as a hedge against currency debasement and inflation, but the ride in 2026 has been anything but smooth.

The Deal Room

M&A / Investments

- Sysco is acquiring Jetro Restaurant Depot for $29.1 billion (including debt), the largest deal in food distribution history. Sysco shares fell ~13% on the announcement as the company plans to take on $21 billion in new debt. (BBG)

- Hg Capital agreed to take enterprise software firm OneStream private for $6.4 billion in an all-cash deal, just two years after OneStream's IPO. Expected to close mid-2026.

Distress / Credit

- Over $4.6 billion in investor capital is now trapped behind withdrawal limits across major private credit funds. Ares, Apollo, Blue Owl, and Cliffwater have all imposed or tightened redemption gates amid rising defaults in the $3 trillion sector. (BBG)

Retirement Lens

There are really only three ways the next few months play out. Each one lands differently on a retirement portfolio.

Scenario 1: The war ends, oil falls, markets bounce. Trump reaches a deal. The Strait reopens, or at least traffic resumes. Oil drops back toward $80. Stocks rally hard off oversold levels. Treasury yields ease further. In this world, the investors who stayed fully allocated get rewarded. Bonds recover. Equities snap back. Gold gives up some of its safe-haven bid, but remains elevated by structural central bank demand. This is the scenario the futures market priced in Tuesday morning, and it is the one most investors are quietly hoping for.

Scenario 2: The war drags on, oil stays above $100, the Fed stays frozen. No deal by April 6. Hormuz remains restricted. Oil grinds between $100 and $120. The Fed holds rates, just as Powell signaled, but inflation runs hot. The OECD's 4.2% forecast starts to look realistic. Equities stay under pressure. Bonds offer decent income at current yields but face price risk if inflation expectations shift. Gold benefits as the hedge it was designed to be. For retirees drawing income, this is the trickiest scenario: your purchasing power erodes slowly while your portfolio treads water.

Scenario 3: Something breaks. Oil spikes above $120. Private credit defaults accelerate. Consumer spending cracks. The Fed is forced to choose between fighting inflation and supporting growth, and either answer is painful. This is the tail risk. It is not the most likely outcome, but it is the one worth stress-testing against. In this world, cash, short-duration bonds, and gold earn their place. Concentrated equity positions and illiquid alternatives become liabilities.

The honest answer is that no one, including Powell, knows which path we are on. What a retirement-focused investor can control is balance: enough equities to participate in a recovery, enough bonds to generate income at today's yields, enough gold to hedge against the scenarios where paper assets stumble, and enough cash to avoid selling anything at the wrong time.

The best portfolio for this week is the one you will not need to touch next week.

Headline Hunt

- The OECD raised its US inflation forecast for 2026 to 4.2%, sharply above the Fed's own estimate of 2.7%, reflecting the energy shock pass-through.

- Iran's parliament approved an early plan to charge tolls on vessels transiting the Strait of Hormuz, including a ban on American and Israeli ships.

- A Kuwaiti crude tanker was struck in what Kuwait Petroleum called an Iranian attack while anchored at Dubai port. No crew injuries were reported.

- February JOLTS job openings data is due today at 10:00 AM ET. January showed 6.9 million openings, little changed from December.

- The tech sector's 50-day moving average crossed below its 200-day, a bearish technical signal. The sector is on pace for its fifth straight monthly loss, the longest streak since 2002.

- Morgan Stanley says the S&P 500 correction is nearing its end stages, pointing to oversold breadth indicators and compressed positioning.

- Strategy (formerly MicroStrategy) reported no new bitcoin purchases last week, snapping a 13-week buying streak.

Recommended Reading

- Why Investors Are Rushing to Exit Private Credit — Bloomberg's deep dive into the convergence of AI-driven software defaults, energy shock, and investor panic across Apollo, BlackRock, and Ares. A clear-eyed look at the first real stress test for the $1.8 trillion sector.

Share with Someone Who'd Value It

If you’ve found The Bull Investor useful, feel free to share it with someone in your circle—perhaps a colleague, a longtime friend, or a family member who takes an interest in their financial future.

We grow best through trusted recommendations, and your referral means a great deal.

Or copy and paste this link to others: thebullinvestor.beehiiv.com