🔹 The biggest IPO ever lands on a nervous market

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

Markets had a good day, and the reason was simple. The threat of a wider war with Iran eased, oil fell, and stocks rallied. The Dow climbed more than 900 points. That is the kind of relief that feels good in the moment.

But underneath it, the harder story has not gone away. Inflation just printed at 4.2 percent, the highest in over two years. The Fed's next move now leans toward a hike, not a cut. And the largest IPO in history is landing on a market still finding its footing.

For anyone thinking about retirement security, days like this are a useful reminder. Relief and resilience are not the same thing.

The Pulse

Two signals matter today. Oil and the war premium attached to it. West Texas crude slipped below $86 a barrel, a near two-month low, after President Trump suggested an Iran deal could be signed as early as this weekend. As that premium drained out, stocks rallied and the dollar's safe-haven bid softened. The fear gauge, the VIX, fell sharply.

The catch is timing. The energy shock already pushed inflation higher last month. So markets are celebrating the exit while still digesting the damage.

Markets

- The S&P 500 rose 1.75 percent to 7,394.30, the Nasdaq gained 2.54 percent, and the Dow added 929.97 points, or 1.86 percent, on Iran de-escalation.

- The move reversed the prior session, when the Dow fell 953 points in its worst day of the year on fresh strike threats.

- Tech, industrials, and materials led the rally, while energy, staples, and real estate lagged as the risk premium faded.

- Crude fell below $86 and Brent toward $89, both near two-month lows, on hopes the Strait of Hormuz reopens.

This was a headline-driven day, plain and simple. The same conflict that knocked markets down on Wednesday lifted them on Thursday. That volatility tells you how much rides on a single negotiation. For long-term investors, the lesson is not to chase the swings, but to notice how fragile the calm still is.

Earnings

The standout was Adobe. It beat expectations, then fell anyway.

- Adobe reported revenue of $6.62 billion, up 13 percent, with adjusted earnings of $5.96 a share, and it raised full-year guidance. Shares still dropped after hours on news that CFO Dan Durn is leaving for Marvell.

- Lennar posted Q2 profit of $305 million, or $1.24 a share, on $7.9 billion in revenue, with home margins compressing to 15.6 percent amid heavy buyer incentives.

- RH, the luxury home-furnishings retailer, released fiscal first-quarter results in a letter from CEO Gary Friedman.

Why it matters. A clean beat that still sells off tells you sentiment is doing the driving, not the numbers. And Lennar's thinning margins are a quiet read on how high mortgage rates keep pressuring housing.

This week's lineup: focus shifts to the Fed's June 16 to 17 meeting, the first under new Chair Kevin Warsh.

Gold & Silver Moves

Gold gave back most of its gains, settling near $4,080 an ounce, its lowest level since November.

That feels strange on a day of geopolitical drama. But the metal is caught between two forces. The war premium that lifted it earlier this year is fading as a deal nears. At the same time, the prospect of a Fed rate hike works against it. Gold pays no interest, so when rates are expected to rise, the cost of holding it goes up.

The longer story remains intact. Central banks keep buying. Poland and China have added steadily, with China now in its eighteenth straight month of purchases. That steady official demand is a floor under the price, even on weak days.

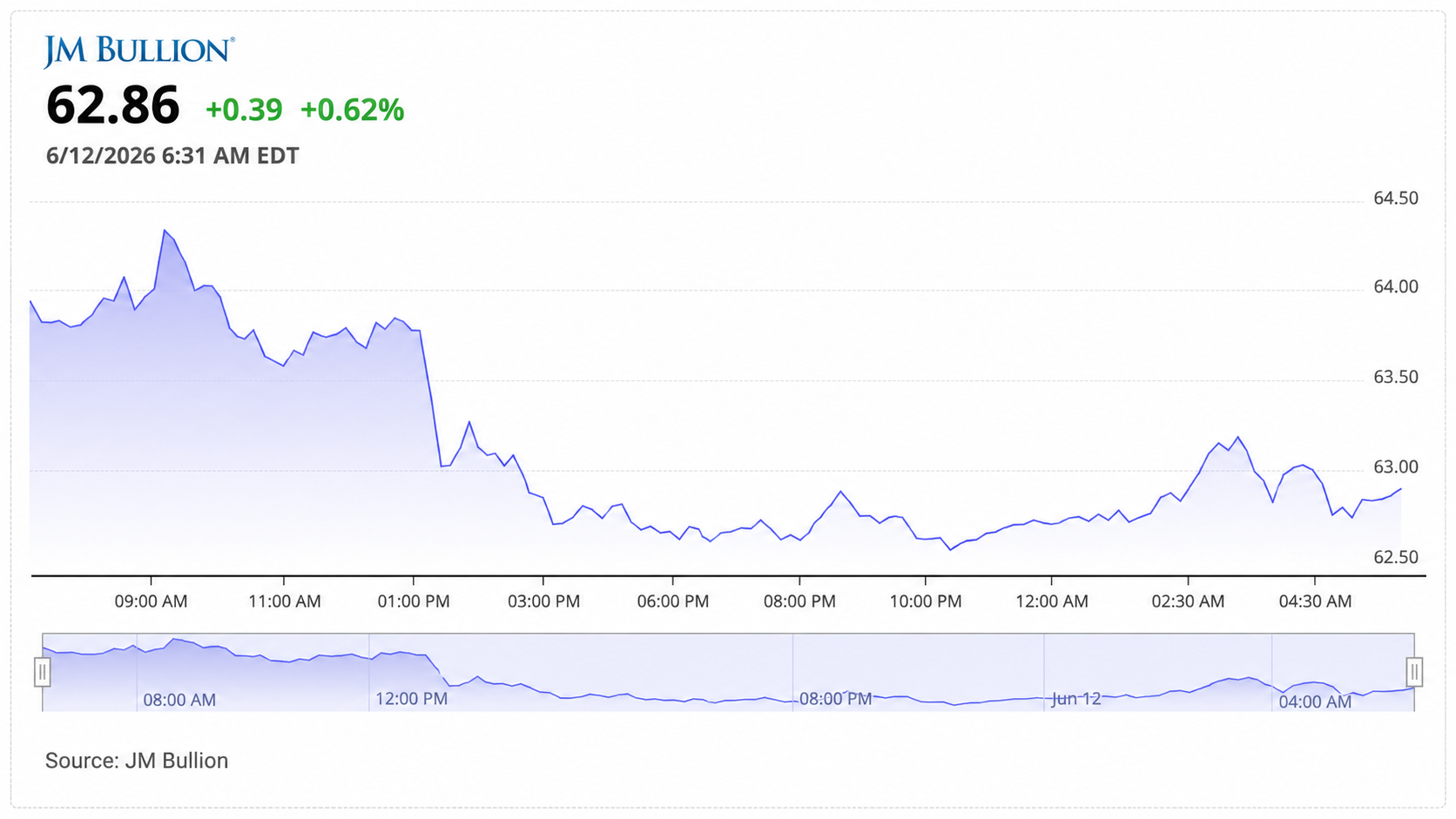

Silver slipped to roughly $63 an ounce, its lowest since December.

Silver tends to fall harder than gold when markets reprice rates, because traders treat it as the more speculative of the two. But it carries a second identity. It is an industrial metal, used in solar panels, electric vehicles, and data centers. That demand is real and growing, even as the financial crowd sells.

The Gold/Silver Ratio: here is where the two metals tell a clearer story together. The gold/silver ratio measures how many ounces of silver it takes to buy one ounce of gold. Right now it sits near 65. Dividing gold's $4,080 by silver's $63 gets you there.

That number has compressed over the past year as both metals climbed. Historically the ratio runs around 60 to 70, and in moments of real fear it spikes above 90 or 100. At 65, silver is not historically cheap against gold. The two are valued more closely than usual.

What does that suggest. A ratio near the low end of its range usually reflects steadier risk sentiment and confidence in silver's industrial demand, rather than a panicked rush into gold as a pure store of value. It says the market is not pricing crisis. If the ratio were to widen back toward 80, that would signal investors retreating into gold's monetary safety. For now, the closeness of the two prices reflects a market that is cautious, not fearful, and one where inflation expectations and industrial appetite are both still in play.

The takeaway. For retirement savers, precious metals are about protecting purchasing power over decades, and a ratio near 65 suggests the usual balance between the two metals is holding, not breaking.

Gold has historically been one of the most private ways to preserve wealth. Here is what some retirement investors are doing about it now.

The Deal Room

M&A / Investments

- Ingredion agreed to take over Tate and Lyle in a deal valued at about $3.6 billion.

- A group of telecom buyers agreed to acquire Patrick Drahi's SFR for roughly $23.5 billion.

IPO / Listings

- SpaceX priced at $135 a share, raising about $75 billion at a $1.75 trillion valuation, the largest IPO in history. It begins trading on the Nasdaq under SPCX on June 12.

- Senator Elizabeth Warren asked the SEC to delay the listing over governance and valuation concerns tied to SpaceX's xAI acquisition. Most observers expect the debut to proceed.

Retirement Lens

Today rewarded patience over panic. The market that fell on Wednesday rose on Thursday, and nothing fundamental changed in between.

For savers near or in retirement, the steadier signals are the ones worth holding onto. Inflation at 4.2 percent erodes fixed income, which is why purchasing power matters more than headline returns. A Fed leaning toward a hike changes the math on bonds and cash. And a market this sensitive to a single negotiation is a reminder that resilience comes from diversification, not from timing the next swing.

None of this is advice. It is context. The job is to stay grounded while the headlines do their dance.

Headline Hunt

- May consumer inflation hit 4.2 percent annually, the highest since April 2023, led by a 40 percent jump in gasoline.

- Wholesale prices rose 6.5 percent year over year in May, the hottest since November 2022.

- The European Central Bank raised rates 25 basis points to 2.25 percent, its first hike since 2023.

- University of Michigan consumer sentiment sits at a record low, with year-ahead inflation expectations near 4.8 percent.

- The EIA said Brent averaged $107 in May, its first monthly decline since December, with Hormuz still largely closed.

- Asian markets followed Wall Street higher overnight, with South Korea's Kospi leading regional gains.

- SpaceX is set for fast-track inclusion in the Nasdaq-100, forcing index funds to buy shares within weeks.

- Bond investors are watching how quickly new Fed Chair Kevin Warsh puts his stamp on policy ahead of next week's meeting.