🔹 The S&P Hit Records. Two-Thirds of Its Stocks Fell.

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

This was a week that reminded investors how much can happen simultaneously. April inflation came in above expectations. The Senate confirmed a new Federal Reserve chair. The S&P 500 hit a record close. Treasury yields pushed to their highest levels of the year. For anyone focused on retirement stability, the message is simple: inflation is not finished, rates are staying higher, and the quality of what you own matters more than the level of the index.

The Pulse

Markets are rising, but the forces pulling against each other — strong earnings, persistent inflation, elevated rates — are not resolving cleanly.

Markets

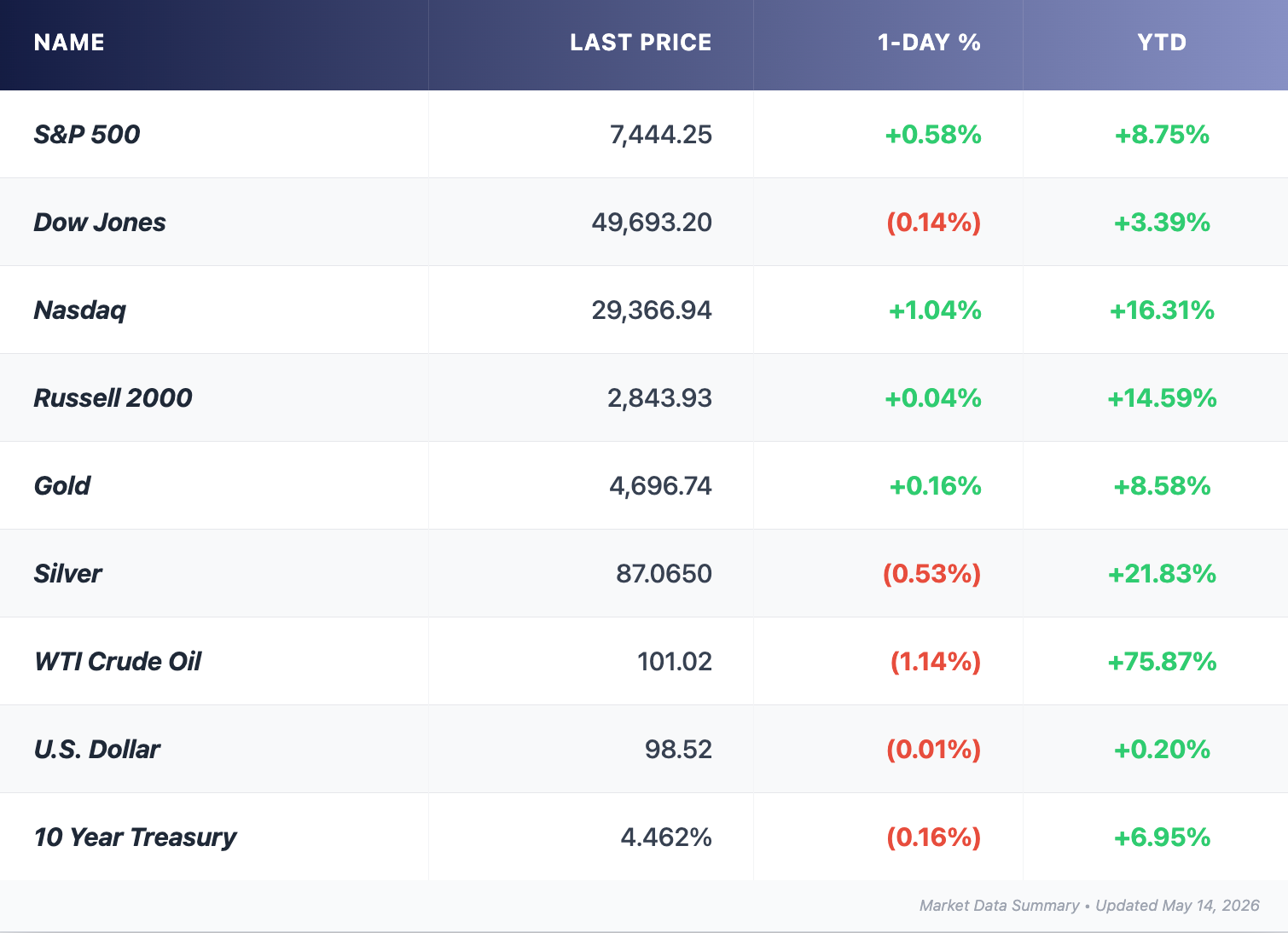

- The S&P 500 rose 0.58% to a record 7,444 on Wednesday. The Nasdaq added 1.2%. The Dow fell 67 points. Roughly two-thirds of S&P 500 stocks closed lower. The gains were narrow, concentrated in semiconductors and AI names.

- April CPI rose 3.8% year-over-year — above the 3.7% forecast and the highest reading since May 2023. Core inflation, excluding food and energy, came in at 2.8%. Producer prices jumped 1.4% for the month, the sharpest monthly increase since March 2022.

- Treasury yields pushed higher across the curve. The 10-year note reached 4.46%, near its 2026 high. The 30-year bond crossed 5%. Yields eased slightly Thursday but remain elevated.

- Year-to-date sector performance tells the real story: Energy is up 21%, Materials up 17%, Industrials up 12%. Technology, despite recent semiconductor strength, remains roughly flat for the year.

Record index levels are masking meaningful weakness. A handful of AI-driven names are carrying the headline number. The rest of the market is navigating elevated costs and rising borrowing rates with more difficulty.

Earnings

- Cisco delivered its strongest quarterly result in years. Q3 revenue of $15.84 billion beat the $15.56 billion estimate. Adjusted EPS came in at $1.06 against $1.04 expected. The bigger news was forward guidance. Cisco raised its full-year AI infrastructure order target from $5 billion to $9 billion and guided Q4 revenue to $16.7–$16.9 billion — comfortably above what analysts expected.

- Alibaba posted its first operating loss since 2021 despite a 40% jump in AI cloud revenue. EPS of $0.19 came far below the $0.84 estimate. The stock rose 7% anyway — investors chose to focus on cloud momentum over the profit miss.

- With 89% of S&P 500 companies reported, 84% have beaten EPS estimates. Blended Q1 earnings growth stands at 27.1% — the strongest since Q4 2021.

Strong earnings remain the market's most important counterweight to rising yields. The bet is that AI-driven productivity justifies elevated valuations even as rates stay higher.

This week's lineup:

Today: Brookfield, Klarna, Figma

Gold & Silver Moves

Gold is trading near $4,700 per ounce, down roughly 0.4% from mid-week. The pressure is a familiar paradox. Inflation data that would normally push gold higher is simultaneously reducing expectations for rate cuts. Higher rates make a non-yielding asset like gold less attractive. The result is a metal that should benefit from its traditional role as an inflation hedge, but is being held back by the yield environment that inflation itself is creating.

India also raised import tariffs on gold and silver from 6% to 15% this week, dampening one of the world's largest physical buying markets.

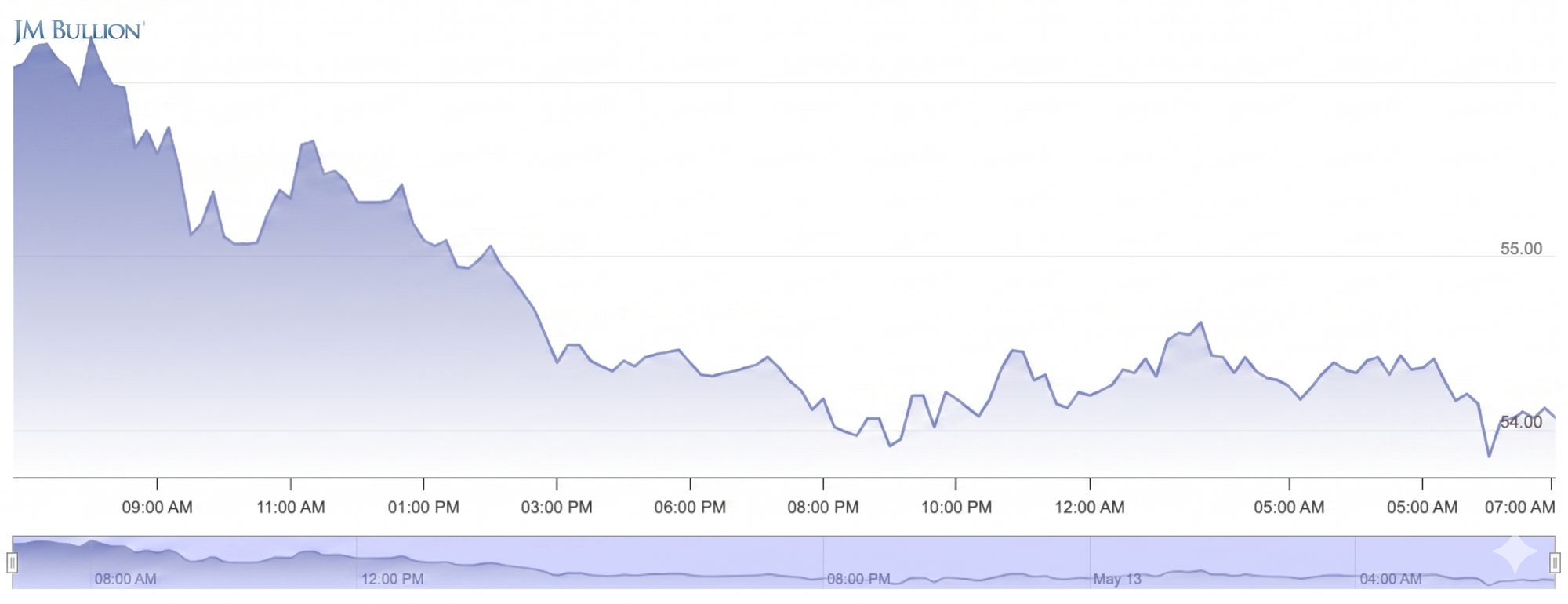

Silver is trading near $87 per ounce, up more than 150% over the past year. Its story differs from gold's in an important way. Industrial demand — driven by AI data centers, solar panels, and electric vehicles — is providing a structural floor that gold simply does not have. Silver's dual role as both an investment and an industrial material is amplifying its gains during this particular cycle.

The Gold / Silver Ratio currently sits near 54. To put that plainly: it takes approximately 54 ounces of silver to buy one ounce of gold. The long-run historical average runs between 65 and 80. A ratio of 54 means silver is priced generously relative to gold by any historical standard.

This compression has been building for months. It reflects the industrial premium being assigned to silver during a period of heavy AI infrastructure investment and energy transition spending. When this ratio falls below 60, it has historically correlated with strong economic activity and elevated risk appetite — both of which are present today.

There is a caution worth noting. Silver is significantly more volatile than gold. It can retrace quickly if industrial demand expectations soften. A ratio near historical lows is not a timing signal, but it does indicate that silver is currently pricing in a great deal of optimism about ongoing capital expenditure in AI and clean energy. If that spending decelerates, the ratio would likely move back toward its long-run average — and silver would fall faster than gold in the process.

For retirement-focused investors, gold near $4,700 represents a stable store of accumulated risk premium, combining geopolitical uncertainty, inflation persistence, and central bank demand into one price. Silver offers more upside if the industrial cycle continues, but carries more downside if it does not. How you weight the two depends on your tolerance for volatility, not just your view on inflation.

Precious metals are doing their job — but the composition of your metals exposure matters as much as the level.

The Deal Room

M&A / Investments

- AMETEK agreed to acquire Indicor Instrumentation for approximately $5 billion in cash. Indicor generates around $1.1 billion in annual sales across industrial and scientific markets. Expected to close in the second half of 2026.

- Roche entered a definitive agreement to acquire PathAI, an AI-driven diagnostics platform, continuing the healthcare sector's consolidation of machine-learning health tools.

- Bullish (NYSE: BLSH) agreed to acquire Equiniti in a $4.2 billion deal, combining its institutional crypto exchange with a regulated transfer agent supporting nearly 3,000 public companies. Deal expected to close January 2027.

Retirement Lens

This week reinforced a pattern that has been building for some time. Inflation is proving stickier than expected. The new Fed chair inherits a divided committee and a deteriorating price environment. Markets are rising, but the gains are narrow and the risks are not.

For investors focused on retirement, the practical priorities remain unchanged. Real assets and inflation-linked instruments serve a purpose in this environment that they did not need to serve in the low-rate decade before. Long-duration positions without strong cash flows carry more risk than they appear to. Patience, diversification, and an honest view of what inflation is doing to purchasing power are the tools that matter most right now.

Nothing here calls for a dramatic change of course. It does call for staying clear-eyed about what is driving gains and what is being quietly eroded.

Headline Hunt

- Kevin Warsh was confirmed as the new Federal Reserve chair in a 54-45 Senate vote, the most partisan confirmation for a Fed leader in US history. His first FOMC meeting is set for June 16-17.

- Boston Fed President Collins warned that additional rate hikes may be needed if inflation fails to abate, adding hawkish commentary on the same day Warsh was confirmed.

- Trump and Xi opened a two-day summit in Beijing covering trade, Taiwan, AI chip exports, rare earths, and Iran, with Apple's Tim Cook, Elon Musk, and Nvidia's Jensen Huang all in the US delegation.

- The IEA warned that global oil markets could remain severely undersupplied until October 2026 even if the Iran conflict ends next month. Saudi Arabia's output has fallen to its lowest level since 1990.

- The UAE formally departed OPEC on May 1, reducing the cartel's effective spare capacity and tightening the structural oil supply outlook for 2027.

- US crude oil inventories fell 4.3 million barrels last week, nearly double expectations, while distillate inventories posted their first increase since March.

- The Philadelphia Semiconductor Index has risen 64% since the end of March, an unusual surge for rate-sensitive technology stocks and a sign that AI earnings expectations are, for now, overriding macro headwinds.

- Netflix's pending $83 billion acquisition of Warner Bros. Discovery and Charter's $34.5 billion merger with Cox Communications remain the two largest pending transactions in the US market.