🔹 While Markets Hit Records, Your Purchasing Power Collapsed

Stocks set fresh records as Hegseth confirms the Iran ceasefire and oil retreats nearly 4%.

Good afternoon,

Here's the dirty little secret Wall Street doesn't want you thinking about: the S&P 500 just hit an all-time high and consumer confidence just hit an all-time low, in the same week. Markets are celebrating. Families are quietly cutting back on furniture, clothing, and cars. Real wages just fell for the first time in three years. And the Federal Reserve's new chairman inherited a mess that could force him to raise rates rather than cut them. If you're within a decade of retirement, or already in it, this is exactly the kind of market that rewards staying informed.

The Pulse

The two-year Treasury yield just hit its highest point in over a year. Markets are up. The pressure underneath is building.

Markets

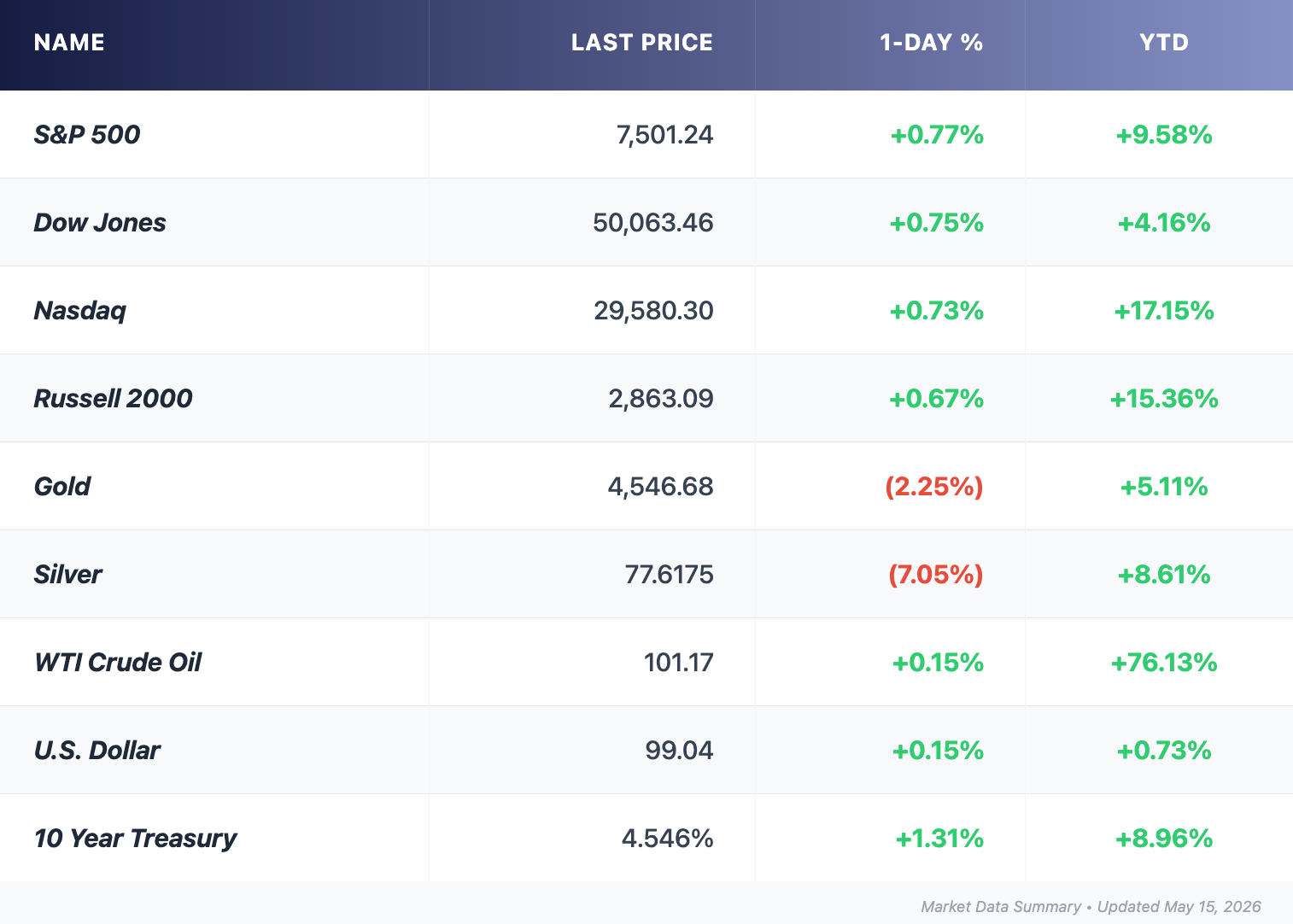

- Thursday's session was one for the history books, on paper. The S&P 500 crossed 7,500 for the first time ever. The Nasdaq added nearly a full percent. The Dow jumped nearly 400 points to reclaim 50,000. The engine: Cisco surged double digits on a blowout earnings report, and Nvidia followed on news that the US approved H200 chip sales to Chinese tech firms.

- The US Commerce Department cleared roughly ten Chinese companies, including Alibaba, Tencent, and ByteDance, to purchase Nvidia's powerful H200 AI chips. Catch: not a single chip has actually been delivered yet. Beijing appears to be quietly telling its companies to hold off.

- April retail sales rose modestly, matching expectations. But here's the fine print: the figures are not adjusted for inflation. Gas prices surged sharply in April. Strip out the gas station receipts and the picture gets thinner. Sales fell at furniture stores, car dealerships, department stores, and clothing shops.

- US futures are slipping slightly Friday after Thursday's record close. The S&P 500 is on pace for its seventh straight weekly gain, the longest such streak since late 2023.

Here's the uncomfortable truth: these records are being made by a handful of AI giants. The companies that serve everyday Americans, retailers, automakers, home goods, are quietly struggling. Two different economies are running at the same time right now. Your portfolio needs to be honest about which one it's actually exposed to.

Earnings

- Applied Materials just reminded everyone that the AI buildout is not a rumor. The semiconductor equipment maker posted record quarterly revenue, comfortably beating Wall Street estimates on both the top and bottom lines. Management said the semiconductor equipment business is now expected to grow more than 30% this calendar year. The company also raised its quarterly dividend for the ninth straight year. Shares climbed after hours.

- AI chipmaker Cerebras Systems exploded on its first day of trading Thursday, closing near a $95 billion market cap. The company is backed by a blockbuster compute deal with OpenAI. It's the biggest pure-play AI IPO in Wall Street history.

- Weekly jobless claims ticked up modestly, slightly above expectations. Continuing claims remain well below historical averages. The labor market is holding, for now.

The AI infrastructure boom is real, it's profitable, and it's accelerating. The question for long-term investors is how much of that story is already priced in.

- Walmart (WMT) reports May 21. Watch what management says about consumer behavior. It will tell you more about the American economy than any index level.

Gold & Silver Moves

Gold is trading near $4,565 per ounce Friday, on track for a weekly loss of roughly 3%. If that sounds strange given that inflation just came in at a three-year high, you're not wrong to be confused. Here's what's happening: gold is caught in a trap of its own making.

Rising inflation is pushing the Federal Reserve toward potential rate hikes. Higher rates make Treasury bonds more attractive. And since gold pays no interest, investors are choosing yield over the traditional inflation hedge, at least this week. Gold is losing a short-term argument it should theoretically be winning.

But step back and this week's price action is noise, not signal. Central banks have been buying gold at a historically elevated pace all year. Inflation is still running near 4%. Geopolitical risk remains elevated with the Hormuz crisis unresolved. None of that changed this week.

Silver settled near $83.60 per ounce Friday, up slightly on the day but pulling back from a recent peak near $88. It held up better than gold this week, and that difference is instructive.

Silver's dual role as both a monetary asset and an industrial metal is acting as a partial buffer. Demand from AI data centers, solar panels, and electric vehicles is providing a floor that gold simply doesn't have. Silver's year-over-year gain dwarfs gold's by a wide margin, a gap that tells a story about industrial cycles as much as it does about inflation.

The Gold / Silver Ratio sits near 55, meaning it takes roughly 55 ounces of silver to buy one ounce of gold. Earlier this week it was closer to 54. The slight widening tells you gold fell harder than silver, and silver's industrial floor held.

The long-run historical average sits between 65 and 80. A ratio near 55 means silver is still carrying a significant premium relative to gold by any historical standard. When this ratio has fallen below 60 in the past, it has typically coincided with strong industrial activity and elevated risk appetite. Both conditions exist today. But the ratio is starting to drift upward, a signal worth watching. If AI spending slows or clean energy investment cools, silver could give back ground faster than gold.

A down week in metals is not a broken thesis. It is a reminder that even sound long-term strategies have uncomfortable moments. Precious metals don't replace income. But in a world where real wages just turned negative and inflation is still running near 4%, they remain one of the more honest stores of purchasing power available to long-term investors.

While we're on the subject of protecting what you've built, there's something happening right now in the banking system that most Americans don't know about yet.

The Deal Room

M&A / Investments

- China agreed to purchase 200 Boeing jets, Trump announced after his meeting with Xi Jinping in Beijing, the first major Chinese aircraft order since 2017. But Boeing's stock fell sharply on the news. Why? Because analysts had been expecting an order nearly three times larger. The market priced in the win; the number disappointed.

- US Treasury Secretary Scott Bessent said China will work "behind the scenes" to help reopen the Strait of Hormuz, noting that Beijing imports more than half its crude from the Middle East and has far more economic incentive to resolve the blockade than Washington does.

IPO / Listings

- Cerebras Systems surged nearly 70% on its first day of trading Thursday, closing near a $95 billion market cap in the largest AI chipmaker IPO on record. Wall Street is already calling it the opening act of a historic wave of AI listings from SpaceX, OpenAI, and Anthropic.

- SpaceX plans to publicly disclose its IPO prospectus as early as next week, potentially targeting what analysts expect could be a record-breaking share sale.

Retirement Lens

Let's be honest about what this week actually said. The headlines celebrated records. The data told a different story. Consumer sentiment hit its lowest point since Harry Truman was president. Real wages fell. Furniture, clothing, and car purchases declined. Gas costs more than 40% above where it was a year ago.

For anyone in or near retirement, those are not abstract statistics. They are the monthly experience of living in this economy. Fixed incomes stretch less. Grocery bills climb. Discretionary spending shrinks first, then necessary spending follows.

Markets at record levels can coexist with real household stress for extended periods. History shows us that repeatedly. The index reflects the earnings of a small number of very large companies. It does not reflect the purchasing power of a retired schoolteacher in Ohio or a former factory worker in Pennsylvania.

This is not a call to panic. It is a call to be honest with yourself about what your portfolio is actually built for. Is it built for income? For inflation protection? For resilience when the consumer finally pulls back harder than the numbers currently show?

The records will get the headlines next week. The fundamentals deserve your attention.

Headline Hunt

- The University of Michigan Consumer Sentiment Index just hit its lowest point in 74 years of tracking, with one-third of Americans spontaneously citing gas prices as their biggest financial concern.

- Trump and Xi jointly agreed that the Strait of Hormuz "must remain open" and Iran "can never have a nuclear weapon," but no formal agreement to end the war was reached and no timeline for reopening the waterway was announced.

- US import prices surged in April at their fastest pace in years, driven by rising fuel costs, adding another layer to an already difficult inflation pipeline before it reaches consumers.

- Real wages fell for the first time in three years in April, as inflation outpaced pay growth, meaning the average American worker took home less purchasing power last month than the month before, even with a paycheck in hand.

- OpenAI and Anthropic are both reportedly targeting IPOs in the second half of 2026 at potential valuations exceeding $1 trillion each, following the validation provided by Cerebras' blockbuster market debut.

- Despite formal US approval of H200 chip sales to Chinese companies, not a single chip has been delivered. Beijing appears to be quietly directing buyers to hold off, leaving a potentially enormous technology deal in limbo.

- Brent crude held above $105 per barrel Thursday as peace talks between the US and Iran remain stalled and the IEA warned that global oil markets could stay severely undersupplied well into autumn.

- Treasury yields climbed to their highest level in over a year this week, a complete reversal from the rate-cut expectations that dominated at the start of 2026.

- National average gas prices are up more than 40% from a year ago, the single biggest factor driving consumer sentiment to its lowest recorded level in the survey's history.